Credit: Zoubeir Souissi/Reuters/Newscom

Environmental groups want an international agreement to include funding for chemical management initiatives in developing countries such as Tunisia, home of this phosphate production plant.

ERROR 1

ERROR 1

ERROR 2

ERROR 2

ERROR 2

ERROR 2

ERROR 2

Password and Confirm password must match.

If you have an ACS member number, please enter it here so we can link this account to your membership. (optional)

ERROR 2

ACS values your privacy. By submitting your information, you are gaining access to C&EN and subscribing to our weekly newsletter. We use the information you provide to make your reading experience better, and we will never sell your data to third party members.

Credit: C&EN/Shutterstock

• Negotiations will open to continue a United Nations program to improve management of chemicals worldwide.

• Industry wants to promote more sharing of chemical hazard and risk information.

• Environmental and health advocates want a levy on chemical production to finance implementation in developing countries.

A key sustainability goal for industry, governments, and environmentalists in 2020 is expanding efforts to improve the management of commercial chemicals.

They plan to build on a United Nations deal called the Strategic Approach to International Chemicals Management (SAICM). The aim of SAICM, which was adopted in 2006 and expires this year, is to ensure that chemicals are manufactured and used in ways that minimize significant adverse impacts on human health and the environment.

To keep global efforts moving in this area, industry, governments, and environmental and health groups will convene in October for the fifth International Conference on Chemicals Management. Their goal is to extend and expand SAICM through 2030.

This meeting is “the top advocacy priority for the chemical industry,” says Michael P. Walls on behalf of the International Council of Chemical Associations (ICCA). Walls is vice president of regulatory and technical affairs at the American Chemistry Council, the largest trade association of US chemical manufacturers.

The global chemical industry has backed SAICM since its inception. Large international companies see it as a mechanism to ensure that all actors in their supply chains are trained and accountable for safe handling of chemicals. They also want to control risks posed by commercial chemicals rather than face regulation or market shifts away from particular compounds.

ICCA wants to expand SAICM to promote the international sharing of hazard and risk information on chemicals, Walls says, especially among developing countries with less-advanced regulatory systems than Canada, the European Union, Japan, and the US. Chemical makers have a great deal of this type of information but have historically kept it in-house.

A voluntary US data-sharing program for chemicals produced in large volumes and information exchange forums in the EU have proved that chemical companies “can find ways to get the relevant information out,” Walls says.

Meanwhile, the International Pollutants Elimination Network (IPEN), a coalition of environmental and health advocacy groups, wants the new SAICM to be stronger than the expiring one, says Joseph DiGangi, the organization’s senior science and technical adviser.

In particular, IPEN is seeking financing to implement SAICM, notably in developing countries. To this end, the coalition is proposing a small levy on chemical manufacturers worldwide, perhaps 0.1% on sales.

In support of the levy, IPEN points to a 2013 UN Environment Programme report that says, “The vast majority of human health costs linked to chemicals production, consumption and disposal are not borne by chemicals producers, or shared down the value-chain. Uncompensated harms to human health and the environment are market failures that need correction.”

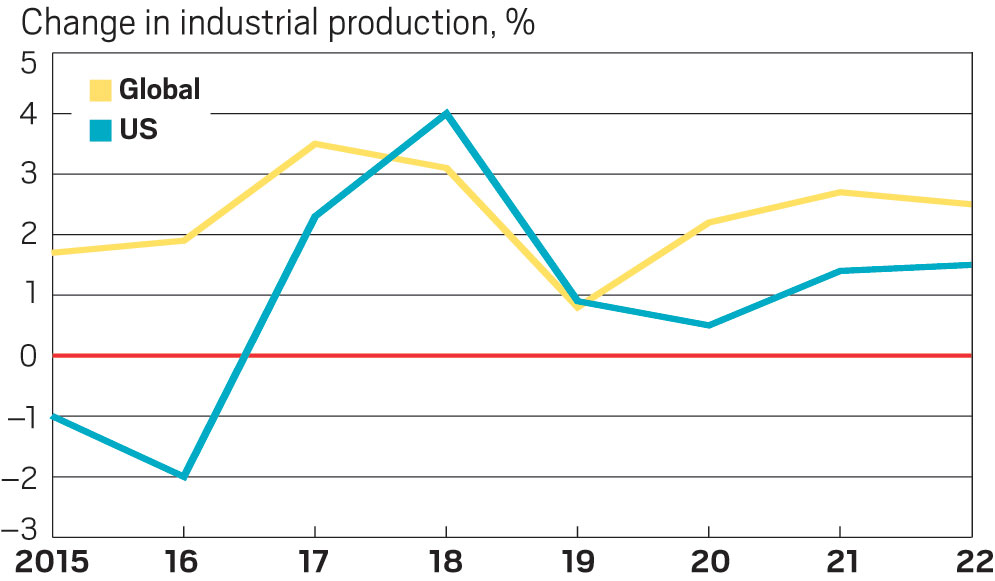

• Growth in demand for chemicals will be negligible this year as manufacturing slows and trade friction lingers.

• US chemical makers will turn to cheap natural gas and new automation tools to stay competitive.

• The industry will look to China for signs of an uptick in industrial manufacturing.

Economists don’t need a crystal ball to predict global industrial growth or recession—they can just check in on recent demand for chemicals.

In the second half of 2019, growth slowed for basic and specialty chemicals used to make industrial goods, like coatings, and durable consumer goods, including cars and electronics.

Add a few quarters’ lag time, and last year’s slowing demand for chemicals presages a dip in overall manufacturing starting early this year. But any downturn is likely to be shallow, and few economists believe the global economy will enter recession territory.

What’s more, growth is likely to tick up in the second half of 2020, according to Oxford Economics. Still, on average, Oxford says, the tally of global growth in gross domestic product will average 2.5% this year and next, a rate the research firm calls “very subdued, even by the standards of the past decade.”

Economic growth in the US will be an even slower 1.8% for 2020, according to a forecast by the American Chemistry Council (ACC), a trade group. That means chemical producers in the US face a lethargic but hardly scary year. Demand from automakers for American-made chemicals will be flat or down, says ACC chief economist Kevin Swift, whereas those used in home construction will finally see an uptick as job and income gains spur the formation of new households.

Overall, growth in US chemical output this year will taper to 0.4% from 0.6% in 2019. But the lull will likely end in 2021, Swift predicts, thanks to the boom in cost-advantaged, shale gas–based production in the US.

To complete the return to more vigorous growth, chemical producers also need a resurgence in spending by industrial manufacturers on raw materials and equipment. That will require secure, lasting trade deals, particularly with China.

Confident US consumers are willing to buy goods, helping boost demand. But here, too, trade is in the way, because tariffs boost prices. Many shoppers will wait until those prices come down.

Growth in manufacturing is expected to slow in the US this year but rebound globally.

Source: American Chemistry Council. Note: Figures for 2019–22 are estimates.

Last month, the Trump administration and Chinese officials said they were nearing a deal on a first-phase trade agreement. But agreements for trade along much of the chemical supply chain will be part of later phases.

In addition to trade deals, chemical firms are watching to see if China allays the deceleration of its manufacturing base, says Duane Dickson, head of Deloitte’s US oil, gas, and chemicals consulting segment.

Meanwhile, Dickson points out, chemical producers have new tools, such as automation and artificial intelligence, to help them cut costs and preserve profits.

“Generally, I have a positive outlook for chemicals, though I’m not saying the worst is over,” Dickson says. “I expect to see the industry come out of this in the first quarter, and then it will take some time to work off excess capacity.”

• Young activists will boost resistance to industrial development.

• Environmental groups are looking beyond oil, gas, and mining to chemical production.

• Pennsylvania and Louisiana are hot spots for industry opposition.

Public pushback against US chemical industry development is expected to ramp up in 2020 as community activists organize to oppose a wave of petrochemical projects moving forward from Texas to Pennsylvania.

“The two hot issues are Cancer Alley and Pennsylvania,” says Wilma Subra, a Louisiana-based environmental scientist and community advocate. She notes that the stretch of her home state between New Orleans and Baton Rouge—the refining and petrochemical region known as Cancer Alley—will see several projects, including a Formosa Petrochemical ethylene cracker and two methanol plants, advance this year. Meanwhile, Shell Chemical is building western Pennsylvania’s first modern ethylene cracker.

Subra, who is involved with communities in both regions, says she has seen an increase in organized opposition to industry development, driven by greater community awareness, increased access to data on the health effects of chemical industry activity, and a new generation of environmental activists. “I call them the hell-raisers,” she says.

Environmental groups, initially focused on other industries, have refocused on chemicals in recent years and anticipate an active 2020. For example, Earthworks, a group that initially targeted only oil and gas, is now also looking downstream. Executive Director Jennifer Krill notes that the prospect of supplying ethane to the Shell cracker has revitalized hydraulic fracturing, or fracking, in western Pennsylvania.

The Ohio Valley Environmental Coalition (OVEC), a group that formed in response to the impact of mining on West Virginia, is increasingly working with communities affected by the chemical industry. The shift was prompted by a spill of (4-methylcyclohexyl)methanol by Freedom Industries into the Charleston, West Virginia, area water system in 2014.

Dustin White, an OVEC project coordinator, points to a coalition of community groups in Pennsylvania, Ohio, and West Virginia called People over Petro. “We need to talk to each other, find out what is happening where, and figure out a broad strategy.”

• The US Congress is considering PFAS legislation that would trigger pollution cleanup obligations.

• The Environmental Protection Agency will announce whether it will establish enforceable drinking-water limits for PFOA and PFOS.

• A court will decide whether to dismiss Chemours’s lawsuit seeking money for PFAS cleanup from DuPont.

This year, both the US Congress and the US Environmental Protection Agency are likely to take action on per- and polyfluoroalkyl substances (PFAS) pollution. These synthetic chemicals, prized for their durability, don’t break down in the environment. Studies of some nonpolymeric PFAS show that they cause health problems in people and laboratory animals.

Last week, the US House of Representatives was set to pass bipartisan PFAS legislation (H.R. 535) after C&EN’s deadline. The bill would speed the cleanup of the two PFAS—perfluorooctanoic acid (PFOA) and perfluorooctane sulfonic acid (PFOS)—that most frequently are detected in US drinking water. Epidemiology studies have linked PFOA and PFOS, chemicals found in the blood of most Americans, to adverse reproductive effects and other health harms.

The bill contains a number of other provisions to control PFAS. At least some of them have sparked opposition to H.R. 535 from industry, including chemical makers, as well as a veto threat from the White House. Sen. John Barrasso (R-WY) told Bloomberg News that the House-passed bill has no chances in the Senate. Barrasso chairs the Environment and Public Works Committee, which controls environmental legislation in the Senate.

Key supporters in the House say they included a raft of provisions in H.R. 535 to create a large platform on which to start negotiations with the Senate on compromise legislation.

The House-passed bill would require the EPA to list all PFAS that contain at least one fully fluorinated carbon as hazardous air pollutants under the Clean Air Act. By law, the agency must stringently regulate emissions of such chemicals.

The legislation additionally would list PFOA and PFOS as hazardous substances under the Comprehensive Environmental Response, Compensation, and Liability Act. This federal law on the cleanup of hazardous waste is also known as the Superfund act. Listing PFOA and PFOS as hazardous substances would require polluters to clean up sites tainted with these chemicals, which formerly were used in firefighting foams and in chemical manufacturing.

Also, the bill would require the EPA to determine, within 5 years, whether any other PFAS should be added to the Superfund list of hazardous substances.

Congress aside, the EPA is plugging away at its February 2019 action plan on PFAS pollution.

The agency announced in December that it had determined whether it will establish legally binding drinking-water standards for PFOA and PFOS. But as of C&EN’s deadline, the decision was undergoing review at the White House and hadn’t been publicly released. The review gives other parts of the government a chance to change or halt the standards.

If the EPA ultimately opts to set health-based limits for PFOA and PFOS, it will take years for the agency to establish national regulations under the Safe Drinking Water Act.

Meanwhile, a legal battle pitting DuPont against Chemours—the fluorochemical manufacturer that DuPont spun off in 2015—is heating up. Chemours says DuPont lowballed the environmental liability the new company would face and is seeking money for PFAS cleanup. Last month, DuPont asked a Delaware court to dismiss the lawsuit. The court is expected to rule soon on the matter.

• European chemical production is expected to show no growth in 2020.

• German chemical production is set to increase marginally in 2020.

• The outlook for the UK chemical industry remains uncertain because of the UK’s exit from the European Union.

European chemical production will show no growth in 2020 after a 1% decline in 2019, according to a downbeat assessment by the European Chemical Industry Council (Cefic), Europe’s largest chemical industry association. The region’s manufacturing sector is strongly exposed to the global economic slowdown and weak manufacturing growth, explains Moncef Hadhri, Cefic’s chief economist.

One notable concern is that economic growth in Germany—for so long a driver of European manufacturing—is fading. This could have knock-on effects across the continent.

Germany’s chemical industry experienced a 7.5% drop in production in 2019 compared with 2018 and is set to grow by just 0.5% in 2020, according to the German Chemical Industry Association (VCI). “Our member companies do not expect their business to improve in the next months,” VCI president Hans Van Bylen said late last year.

VCI blames its members’ struggles on a global economic slowdown exacerbated by trade disputes between China and the US. One of the fallouts is that Germany’s auto industry—Europe’s largest and a key end market for European chemical companies—is shrinking. Globally, the sector is set to produce 4 million fewer cars in 2019 than in 2018 and won’t return to the 2017 peak of 84.4 million vehicles for at least 4 years, according to the Center Automotive Research at the University of Duisburg-Essen.

Predicted growth in Germany’s domestic chemical sales in 2020

Predicted producer price change for chemicals sold in Germany in 2020

Source: German Chemical Industry Association.

Meanwhile, the UK’s planned exit—or Brexit—from the European Union by Jan. 31 will potentially jolt Europe’s chemical industry. Divorce terms between the UK and the EU had not been settled by C&EN deadline, but they could lead to new tariffs, delays of shipments at UK-EU borders, and uncertainty around compliance with EU chemical regulations. These factors, in turn, could cause companies to take their business out of the UK to continental Europe. “In the midterm, the question is, ‘Will people continue to invest in the UK?’ That is a big concern,” says Mark Porter, head of chemicals for the consulting firm Bain.

Amid the worries lie a few positive signs for Europe’s chemical industry, including indicators that one of the sector’s main markets—the construction industry—should grow this year, Hadhri says.

And in a period of global oversupply for basic petrochemicals, Porter sees a silver lining for the ethylene crackers in Europe that produce them: they are older than in other regions, meaning most of them are already paid for. Some European firms are also in the process of reducing their feedstock costs by importing low-cost, shale-derived natural gas from the US. With this strategy in mind, the British firm Ineos is building in Antwerp, Belgium, Europe’s first new cracker in 20 years.

• Consumer product firms are committed to using more than 5 million metric tons of recycled plastic in their packaging annually by 2030.

• Europe will lead the way on plastics recycling legislation.

• More than 60 technologies for recycling plastic are in development.

Public awareness that plastic waste is everywhere—including the oceans and our food—will pressure producers to take action this year. Analysts say plastics firms will accelerate their shift into recycling by forging partnerships with plastics collection and recycling firms, testing nascent technologies, and even planning commercial plants.

“There is growing momentum behind this. There is a shift in consumer attitude that I don’t think will reverse itself,” says Mark Porter, head of chemicals for the consulting firm Bain.

Europe is at the forefront of plastics recycling policy, with a single-use plastics ban in place and ongoing efforts to recycle 55% of plastic packaging by 2030, but momentum to recycle is becoming global. India is considering new laws to drive up recycling and has already introduced legislation banning single-use plastics in certain applications. In the US, state legislation will move ahead in 2020, notably with California aiming for new plastics recycling requirements for manufacturers.

European Union’s 2025 target for annual plastics recycling

European Union’s current level of annual plastics recycling

Source: European Commission.

Major consumer product companies, such as Coca-Cola, Nike, and Unilever, are also pushing for more recycling. Coca-Cola has publicly stated that 50% of its plastic packaging will be recycled material by 2030. Collectively, leading consumer product companies are committed to using between 5.0 million and 7.5 million metric tons (t) of recycled plastic annually by 2030, according to a report by Closed Loop Partners, an investment firm focused on the circular economy.

A number of major chemical companies say they will be advancing technologies in 2020 to convert postconsumer mixed plastic waste into useful chemicals. More than 60 technologies are in development, Closed Loop Partners says in a recent report. At present, however, little beyond traditional mechanical recycling of plastics is practiced on a commercial scale.

Pieterjan Van Uytvanck, principal sustainability analyst for the consulting firm Wood Mackenzie, says that “2020 is set to be another busy year for the transition from virgin to recycled plastic production, but companies are starting small.” With global production of virgin polypropylene, polyethylene, and polyester reaching 260 million t in 2019, he says, “it is a transition that will take decades.”

• Mechanical: The shredding, washing, and melting of plastics to make new material. A simple approach limited by waste quality and type.

• Solvent purification: A dissolution process in which plastics such as polystyrene are dissolved and purified using solvents.

• Pyrolysis: The decomposition of plastics in the absence of oxygen, typically under pressure and above 430 °C. The product is an oil that can be reused to make plastic.

• Depolymerization: The conversion of polymers into monomers via processes such as glycolysis and hydrolysis. The monomers can be repolymerized.

• Gasification: The heating of plastics at high temperatures to break chemical bonds and form synthesis gas, a feedstock for making new polymers and other chemicals.

Sources: PlasticsEurope, Closed Loop Partners.

• Regulators are considering new bans and restrictions on pesticides such as chlorpyrifos and dicamba.

• In the US, federal regulatory action may broaden the allowable use of some pesticides.

• Environmental and health advocacy groups are putting pressure on major food brands and retailers to enact their own policies to reduce the use of pesticides.

US agriculture’s reliance on pesticides—and their effects on pollinators, the environment, and human health—garnered headlines in 2019. This year will bring additional attention to tactics for reducing the use of pesticides as part of a broader effort to make agriculture and food systems more sustainable.

Pesticides in the news include glyphosate, the subject of thousands of lawsuits claiming that heavy, routine use contributed to cancer. Researchers have fingered neonicotinoid insecticides as harmful to pollinators. And farmers in the US Midwest say widespread use of dicamba herbicide is damaging valuable crops because of the chemical’s tendency to drift.

Until recently, the only constraint on the use of pesticides has been regulation. And under the Trump administration, federal regulatory action on pesticides has slowed, stalled, or even reversed.

Now, in some cases, states are stepping in. For example, Arkansas has prohibited farmers from spraying dicamba after May 25 this year. California, Hawaii, and New York are phasing in bans on the insecticide chlorpyrifos.

Activist groups are pursuing a different angle. They started by asking big-box hardware stores and garden retailers to drop insecticides containing neonicotinoids. Now they are demanding that food brands and retailers craft policies requiring farms that supply them to track and limit their use of pesticides.

In November, the environmentally focused investor organization As You Sow issued a report that ranked 14 leading food brands on whether their sustainable sourcing guidelines, if they exist, include goals for measuring and reducing pesticide use. General Mills and PepsiCo received the highest rankings with scores of 18 and 14 out of 30, respectively. The remaining dozen firms scored less than 10.

Similarly, Friends of the Earth, another environmental group, has reached out to grocery chains asking them to protect pollinators with policies that encourage responsible use of pesticides on fruits and vegetables. So far Aldi, Costco, and Kroger have launched pollinator policies.

For now, food brands are still getting up to speed on basic facts about pesticides in their supply chains, says Rod Snyder, president of Field to Market, an alliance of agriculture stakeholders. The alliance’s sustainability tool, Fieldprint, does not track pesticides but may in the future.

“We are seeing a growing desire on the part of food companies for supply chain information on pesticides,” Snyder says. In addition, he emphasizes that brand-based supply chain programs must work with farmers directly to reward favored pest management practices.

• The Environmental Protection Agency must finalize risk evaluations for 10 chemicals under the Toxic Substances Control Act.

• Environmental and public health groups are likely to challenge the EPA’s risk evaluations if the agency ignores certain uses.

• The EPA will decide whether to strengthen current airborne fine particulate matter and ground-level ozone standards under the Clean Air Act.

The US Environmental Protection Agency has its work cut out for it this year. Under the Toxic Substances Control Act (TSCA), the agency faces a June deadline to finalize risk evaluations for 10 chemicals already on the market. The agency must also begin reviewing an additional 20 high-priority chemicals in order to complete those evaluations within 3–3½ years. On top of that, the EPA is expected to evaluate the risks of two phthalates—diisononyl phthalate and diisodecyl phthalate—as requested by manufacturers.

The EPA has been evaluating the first 10 chemicals since TSCA was revised in 2016. It has yet to release draft assessments for four of them, including two particularly controversial substances: asbestos and trichloroethylene. The agency plans to publish those drafts early this year to give stakeholders and its TSCA advisory committee time to provide input before the June deadline. Once the EPA finalizes all 10 reviews, the agency will have 2 years to issue regulations to manage any risks to human health and the environment it determines are unreasonable.

The six draft assessments that the EPA has released have garnered criticism from the TSCA advisory committee and environmental groups, which claim the agency lacks toxicity data to support its conclusions. Critics also point out that the EPA is ignoring risks to the general population.

The draft evaluations “have excluded sources of exposure, such as drinking water contamination, air emissions and use of personal care products, that are harmful to health and the environment,” Bob Sussman, counsel for the advocacy group Safer Chemicals, Healthy Families, says in a statement.

The EPA is likely to face more criticism and lawsuits if it does not change its approach. A federal appeals court ruled late last year that environmental groups can challenge the EPA’s final risk assessments if the agency underestimates risks by ignoring certain uses of chemicals.

The Environmental Protection Agency must issue final risk assessments for these 10 substances by June. Before it can do so, it must release draft evaluations that are reviewed by an advisory committee.

| Name of Substance | Draft evaluation release | Advisory committee meeting | Advisory committee report | Final assessment release |

|---|---|---|---|---|

| Asbestos | ||||

| 1-Bromopropane | ||||

| Carbon tetrachloride | ||||

| 1,4-Dioxane | ||||

| Hexabromocyclododecane and other cyclic aliphatic bromide flame retardants | ||||

| Methylene chloride | ||||

| N-Methylpyrrolidone | ||||

| Pigment violet 29 | ||||

| Tetrachloroethylene, also known as perchloroethylene | ||||

| Trichloroethylene |

Name of Substance: Asbestos

Draft evaluation release:

Advisory committee meeting:

Advisory committee report:

Final assessment release:

Name of Substance: 1-Bromopropane

Draft evaluation release:

Advisory committee meeting:

Advisory committee report:

Final assessment release:

Name of Substance: Carbon tetrachloride

Draft evaluation release:

Advisory committee meeting:

Advisory committee report:

Final assessment release:

Name of Substance: 1,4-Dioxane

Draft evaluation release:

Advisory committee meeting:

Advisory committee report:

Final assessment release:

Name of Substance: Hexabromocyclododecane and other cyclic aliphatic bromide flame retardants

Draft evaluation release:

Advisory committee meeting:

Advisory committee report:

Final assessment release:

Name of Substance: Methylene chloride

Draft evaluation release:

Advisory committee meeting:

Advisory committee report:

Final assessment release:

Name of Substance: N-Methylpyrrolidone

Draft evaluation release:

Advisory committee meeting:

Advisory committee report:

Final assessment release:

Name of Substance: Pigment violet 29

Draft evaluation release:

Advisory committee meeting:

Advisory committee report:

Final assessment release:

Name of Substance: Tetrachloroethylene, also known as perchloroethylene

Draft evaluation release:

Advisory committee meeting:

Advisory committee report:

Final assessment release:

Name of Substance: Trichloroethylene

Draft evaluation release:

Advisory committee meeting:

Advisory committee report:

Final assessment release:

| Note: As of Jan. 6, 2020. |

The EPA must also ensure that new chemicals do not pose unreasonable risks to human health and the environment. In a typical year, the agency receives 500–600 requests from manufacturers to market new chemicals. As of Dec. 1, 2019, the EPA had 374 new chemicals under review. The agency plans to overhaul its approach for evaluating new chemicals this year to address some stakeholders’ concerns and to get new chemicals onto the market in a timely fashion.

In addition to TSCA requirements, the EPA faces Clean Air Act deadlines this year to either strengthen the limits for airborne fine particulate matter and ground-level ozone or explain why changes are not justified. The agency must do so with advice from an advisory committee that has access to less expertise than in the past. Last year, the committee recommended no change to both the fine particulate matter and ozone limits. However, EPA staff and an independent panel of reviewers recommended lowering the limit for fine particulate matter to protect public health. The EPA must now decide how to balance the divergent views.

• An ebbing of the trade war will be good for China’s chemical industry.

• Closing polluting plants will benefit remaining firms.

• Thanks to a new law, foreign companies are investing in wholly owned plants in China.

Despite uncertainty caused by a slowing economy and the trade war with the US, China’s chemical industry has reasons to anticipate a brighter 2020, analysts say.

On Dec. 13, China and the US reached a deal to avoid a new round of tariffs. Both sides promised to partially phase out some import tariffs that were imposed after the Trump administration launched the trade war in mid-2018. Chemicals and other products were hit with tariffs of as high as 25% in several rounds of hostile exchanges between the two world powers.

Both sides have felt the impact. From January through October 2019, US chemical exports to China fell 3% compared with the same period a year earlier, landing at $13.3 billion. Meanwhile, Chinese chemical exports to the US dropped more than 20% to $14.1 billion, according to the US Census Bureau.

China’s slowing economy—the country’s growth rate was 6% in the third quarter of 2019, the slowest in decades—also reduced demand for chemicals.

Although the trade war truce has yet to relieve tariff burdens on chemicals, other changes will play a positive role this year.

As a result of government efforts in recent years to shut down high-polluting manufacturers, prices in China for many chemicals are buoyant. “Therefore, most major chemical companies should enjoy rather satisfactory profit margins in the coming years,” says Ye Yingmin, president of the Beijing-based consulting firm Chem1.

In addition, China’s chemical economy seems to be rebounding. According to the National Bureau of Statistics, the output of China’s chemical industry increased by 7.9% in November over the previous November, higher than the 4.4% gain for the year to date.

A silver lining from the trade war is that non-Chinese chemical firms are investing in China, sometimes with an eye to avoiding tariffs. The trend is aided by government efforts to further open China’s market, says Kelly Cui, a China-based senior analyst with the consulting firm Wood Mackenzie. BASF, ExxonMobil, and Sabic all have signed multibillion-dollar deals to develop wholly owned chemical facilities in China.

• Government officials want to protect university research from foreign interference.

• Scientists fear that restrictions will hinder scientific collaboration and progress.

Throughout 2019, the US Congress, law enforcement, and intelligence agencies expressed fears about the security of research at US universities. In particular, they pointed to Chinese efforts to steal research by secretly hiring US scientists. Those fears have prompted a series of efforts that could result in new security recommendations in 2020.

Decrease in international enrollment in US graduate schools for the 2018–19 school year, the second straight year of decline

Source: Institute of International Education, Open Doors, 2019.

One provision in the 2020 National Defense Authorization Act would require the White House Office of Science and Technology Policy (OSTP) to look at ways to protect federally funded science from foreign threats. Another would ask the National Academies of Sciences, Engineering, and Medicine to examine the balance between national security and international collaborations.

The OSTP has has been holding meetings with the research community to talk about security concerns. Scientists are worried that restrictions on traditionally open research will hurt US science. Even in areas of fundamental scientific research that do have national security implications, “we wall such research in at our own peril,” says Tobin Smith, vice president for policy at the Association of American Universities. “In many of these areas, China and other countries are making advances that we need to know about.”

A recent report by the defense advisory group Jason says that the risk of hindering scientific advancement is greater than any potential national security benefits. Jason suggests expanding research integrity rules to include disclosure of foreign funding or commitments that would cause a conflict of interest. The National Institutes of Health and other US agencies have already issued clarifications for reporting foreign contacts.

US scientists are worried that research limits, combined with anti-immigrant rhetoric and visa restrictions, are creating the perception that the US isn’t welcoming to international scientists. A National Academy of Sciences report on the future of atomic, molecular, and optical physics recommends creating more mechanisms for international collaborations, not fewer.

Atomic, molecular, and optical science “has been very successful in the US because of an open collaborative model,” says report cochair Nergis Mavalvala from the Massachusetts Institute of Technology. “These are very important issues in realizing the full potential of what the scientific community can achieve.”

Saudi Arabia’s national oil company, Saudi Aramco, just had an initial public offering on the Saudi stock exchange, the largest in history, that valued the company at $1.7 trillion. The IPO is the centerpiece of the Saudi government’s plan to modernize its economy by redeploying capital into high-growth sectors and away from oil and gas.

One of those target sectors is chemicals. Aramco has unveiled new projects around the world as part of its goal of spending $100 billion on the industry. Additionally, it is buying into two of the world’s largest chemical makers, Saudi Arabia’s Sabic and India’s Reliance Industries.

• $6 billion ethylene plant at its South Korean S-Oil affiliate

• $8 billion ethylene and aromatics plants at its Motiva Enterprises subsidiary in the US

• $9 billion petrochemical complex in Saudi Arabia with Total

• $44 billion refining and petrochemical complex in India with Indian Oil and other partners

Sources: Company reports.

2018 revenue

2018 daily production of oil and natural gas liquids, more than the combined total of ExxonMobil, BP, Chevron, Shell, and Total

Chemical capacity in 2018

Expected chemical capacity in 2020

Stake it is purchasing in the chemical and refining business of Reliance Industries, the world’s 11th-largest chemical company

Stake it is purchasing in Sabic, the world’s 4th-largest chemical company.

Sources: Company documents.

• A wave of big US ethylene expansion projects will wrap up in 2020.

• The new petrochemical capacity may pinch profitability over the short term.

• The pace of US cracker projects may slow because of global oversupply.

Over the past 3 years, petrochemical makers started up nine new ethylene crackers in the US with a combined annual capacity of nearly 10 million metric tons. The projects, meant to take advantage of cheap and plentiful ethane derived from shale gas, have expanded US capacity for the basic chemical by about 30%.

Five of the projects started up in the past year and are currently ramping up production. The biggest is Sasol’s complex in Lake Charles, Louisiana, which includes ethylene, polyethylene, α-olefin, and alcohol plants. The project ended up costing $12.9 billion, about $4 billion over budget, and led to the ouster of the company’s co-CEOs.

Two more projects—a modest Dow expansion and a joint venture among Total, Nova Chemicals, and Borealis—are scheduled to begin operations this year.

After nine start-ups between 2017 and 2019, a new wave of petrochemical projects is in the works.

| Company | Location | Start-up Date |

|---|---|---|

| Borealis, Nova Chemicals, and Total | Port Arthur, Texas | 2020 |

| Dow | Freeport, Texas | 2020 |

| ExxonMobil and Sabic | San Patricio County, Texas | 2022 |

| Chevron Phillips Chemical and Qatar Petroleum | US Gulf Coast | 2024 |

| Shell Chemical | Monaco, Pennsylvania | early 2020s |

| Daelim Industrial and PTT Global Chemical | Belmont County, Ohio | n.d. |

| Formosa Petrochemical | St. James Parish, Louisiana | n.d. |

| Motiva Enterprises (Saudi Aramco) | US Gulf Coast | n.d. |

| ExxonMobil | Appalachia | n.d. |

Company: Borealis, Nova Chemicals, and Total

Location: Port Arthur, Texas

Start-up Date: 2020

Company: Dow

Location: Freeport, Texas

Start-up Date: 2020

Company: ExxonMobil and Sabic

Location: San Patricio County, Texas

Start-up Date: 2022

Company: Chevron Phillips Chemical and Qatar Petroleum

Location: US Gulf Coast

Start-up Date: 2024

Company: Shell Chemical

Location: Monaco, Pennsylvania

Start-up Date: early 2020s

Company: Daelim Industrial and PTT Global Chemical

Location: Belmont County, Ohio

Start-up Date: n.d.

Company: Formosa Petrochemical

Location: St. James Parish, Louisiana

Start-up Date: n.d.

Company: Motiva Enterprises (Saudi Aramco)

Location: US Gulf Coast

Start-up Date: n.d.

Company: ExxonMobil

Location: Appalachia

Start-up Date: n.d.

Sources: Company documents.

Note: n.d. means not disclosed.

With all the new capacity for ethylene and derivatives coming on line, petrochemical makers report slimming profits. Dow’s packaging and specialty plastic unit saw an 18% operating profit decline for the first 9 months of 2019. One contribution, the firm said, was a slumping ethylene market due to the new capacity. LyondellBasell Industries registered a 19% profit decline for its North American olefin business over the same period.

John Maselli, a research analyst at the consulting firm Wood Mackenzie, expects North American petrochemical sales to be strong in 2020, mostly because of exports of products such as polyethylene. However, he thinks the ethylene industry will continue to face overcapacity. “I don’t see relief quite yet,” he says.

Seven new projects are being kicked around for the years beyond 2020. Only two, Shell’s in Pennsylvania and an ExxonMobil-Sabic joint venture near Corpus Christi, Texas, are under construction.

Maselli says the industry is “hitting the pause button” on a new wave of expansions, even though the feedstock resources are available to support new crackers. The problem, Maselli says, is large projects in Asia, China in particular. Over the previous 5 years, Chinese chemical producers have been making good enough profits to justify expansions that will create overcapacity in global markets toward the middle of the decade.

• Electric vehicle sales will ramp up to meet greenhouse gas reduction targets.

• Demand will rise for lithium chemicals and membrane separators as the market shifts to vehicles more dependent on batteries.

• Plastics will play a bigger role to reduce weight and increase vehicle range.

Electric vehicle sales will likely rise in the US this year, driven by global warming concerns and associated regulatory mandates, industry observers say.

Overall, US light-vehicle sales will slip 2.3% to 16.5 million units in 2020 compared with 2019, according to the American Chemistry Council (ACC), a trade association. The ongoing economic slowdown accounts for this general decline.

In contrast, the consulting firm IHS Markit predicts that the percentage of US electric vehicle sales—including fuel-cell and hybrid-electric units—will more than double, from roughly 4% of overall vehicle sales in 2018 to 9% in 2020. Europe and China will see electric car sales surge from 6% of overall 2018 sales in each region to 23 and 19%, respectively, in 2020. Behind the increases are fleet carbon dioxide reduction targets in California and similar greenhouse gas reduction requirements in Europe and China.

Kevin Swift, the ACC’s chief economist, can’t say if the overall chemistry content of electric vehicles—now $3,335 per vehicle—is higher than in internal combustion vehicles. But Swift does say the mix of chemicals used in electric vehicles is different. For instance, expect to see an increase in lithium chemicals and polymer separators used in battery-powered vehicles, he says.

The move to electrification also gives automakers “an opportunity to reengineer their vehicles and reduce mass,” says Michael Robinet, executive director of IHS Markit’s Automotive Advisory Services. The use of more plastics in door panels and substitution of plastic composites for steel and aluminum structural components will reduce vehicle weight and help increase battery range, he says. And because electric vehicles operate at hundreds of volts—up from the 12 V typical of internal combustion vehicles—he sees growing demand for high-heat-resistant plastics and associated chemical additives.

Refrigerants will still be required to remove heat from both passengers and battery packs in electric vehicles. But overall they will need fewer chemical fluids than internal combustion vehicles, Robinet tells C&EN. So the shift to “electrically driven propulsion” means that cars will depend less on brake fluids, engine oil, and fuels like gasoline and diesel, he points out.

• The US Food and Drug Administration is likely to crack down on cannabidiol products that claim to treat specific diseases or are marketed to children.

• Regulatory uncertainty will create risks for firms seeking to market CBD-containing products in the US.

Cannabidiol (CBD), a chemical found in cannabis, is popping up in all sorts of consumer products sold in the US, including lotions, tinctures, dietary supplements, food, beverages, and pet food. The US Food and Drug Administration has for several years been pondering ways to make it legal to market CBD in products regulated by the agency.

Most of the CBD in products sold in the US today is derived from hemp, a cannabis strain that contains less than 0.3% of the psychoactive ingredient tetrahydrocannabinol, or THC. Nevertheless, the majority of such products are illegal because they don’t comply with the Federal Food, Drug, and Cosmetic Act.

The FDA said late last year that it does not consider CBD generally recognized as safe for use in human or animal food, so it can’t be legally added to food without premarket approval from the FDA. The agency also said it is illegal to add CBD to food because it is an active ingredient in the epilepsy drug Epidiolex. For the same reason, CBD does not meet the definition of a dietary supplement.

To overcome these problems, Congress in December directed the FDA to develop an enforcement discretion policy for products containing CBD. Such a policy could allow companies to sell CBD in dietary supplements and foods without penalty. In addition, the bill directs the FDA to determine the extent of mislabeled or adulterated CBD products currently in the US marketplace.

In the meantime, the FDA is likely to crack down on manufacturers of CBD products that claim to treat particular diseases, are marketed to children, or are sold in more than one US state.

The FDA has concerns about the safety of CBD, including the potential for liver injury and interactions with other drugs. The agency has also received “reports of products containing contaminants, such as pesticides and heavy metals,” FDA principal deputy commissioner Amy Abernethy says in a November statement.

That leaves big questions and risks for manufacturers of CBD products, many of which thought the 2018 US farm bill gave them a green light to market their products in the US. Until the FDA’s enforcement discretion policy is in place, lawyers say, the only safe bet is to market CBD in cosmetics, which the FDA allows without premarket approval, and to avoid making health claims.

• The drug pipeline is dominated by companies requiring contract manufacturing services.

• Funding for biotech remains strong.

• The sector needs to digest recent investments.

• Big pharma continues to off-load manufacturing.

As much as industry watchers might welcome a break in the monotony, 2020 is likely to be another up year for the pharmaceutical services sector. Gains, however, may fall short of the double-digit growth of recent years.

"Our sense is there have been some signals [of a slowdown], but they are pretty minor ones," says John Kreger, a health-care analyst at the investment bank William Blair. "Fund flows into biotech have been strong on an absolute basis but down each of the first three quarters" of 2019 compared with 2018. Growth in the pharmaceutical pipeline was also slower.

"These things translate into 2020 being a good year," Kreger says, "but maybe not as strong as 2019 and 2018."

James Bruno, president of the consulting firm Chemical and Pharmaceutical Solutions, agrees. "Most companies are at full capacity right now, and that should continue through most of the year." The high level of investment in recent years may eventually become a drag, he notes, if demand for services slows.

"Demand for good contract manufacturers continues to be strong," says Stephan Haitz, president of CDMO sales and marketing at the service firm Cambrex. Over half of drug candidates in the pipeline are from "non-top-30" drug companies, he says, including many virtual firms that lack manufacturing capabilities. Big pharma, Haitz adds, continues to divest manufacturing plants.

Some service companies see shifts in customers' technical requirements as a harbinger of a good year ahead. "People recognize value and quality, and because of that they are turning to companies in the West, mostly in the US," says Aslam Malik, CEO of SK Pharmteco, a US-based division of the South Korean conglomerate SK.

Rudolf Hanko, former CEO of the Swiss pharma services firm Siegfried, is optimistic for continued strength in the sector. He sees room for growth as investors pressure drug companies to improve capital efficiency, leading them to outsource more production.

An interest rate rise, however, would spell trouble for an industry with high debt levels, Hanko cautions. "Nobody knows when the bubble will burst, but everyone knows we are already in a bubble. There is quite some leverage in the industry."

• Analytical instrument makers will continue to invest in the diagnostics market.

• Developing regulatory know-how will be key to instrument makers' diagnostics advances.

• Government and insurance company pricing pressures could limit diagnostics profitability.

Scientific instrument makers have been moving into the clinical diagnostics market for years, and that's a trend likely to continue, industry veterans say. It's a path away from traditional analytical science markets but not one that will lead to neglect, they say.

Among the major instrument makers, interest in diagnostics goes back to acquisitions such as Thermo Fisher Scientific's 2011 purchase of the allergy diagnostics maker Phadia, and Agilent Technologies' 2012 buy of the cancer diagnostics specialist Dako. In November, press reports indicated that Thermo Fisher was among those bidding for the Dutch diagnostics maker Qiagen. Though Qiagen has decided to remain independent, the addition of the Dutch firm, which has annual sales of $1.5 billion, could have added heft to Thermo's nearly $4 billion-per-year specialty diagnostics business.

David B. Patteson, CEO of the mass spectrometer maker Advion and an operating partner at the private equity firm Ampersand Capital Partners, says he can understand the attraction of the diagnostics market, where mass spectrometers are increasingly being used. While the more mature analytical instrument business grows at about 4–5% a year, the clinical diagnostics business is growing at or near double-digit rates, he says.

"It's an easy pivot once an analytical firm develops the regulatory know-how needed to be a diagnostics player," Patteson says. "I don't think it's a destructive pivot," he adds, calling the two markets "kissing cousins."

"The trend of top vendors moving into diagnostics will continue and accelerate," predicts Rohit Khanna, a former executive at the instrument maker Waters and now an independent consultant. Up-and-coming mass spectrometry identification of disease-predicting biomarkers is superior to the amino acid affinity assays widely used today, he says.

Terrence Kelly, an operating partner at the private equity firm SFW Capital Partners and former president of Waters's TA Instruments division, agrees that diagnostics is a growing business for analytical instrument makers. But he points out that pricing pressure from governments and insurance companies could ultimately put a damper on sales growth and profits.

By 2030, hydrogen could be on its way to being a clean, affordable, carbon-free gas that serves traditional chemical and refining customers as well as new customers that use it to generate electricity, heat homes, and fuel cars, according to the International Energy Agency (IEA). But that's only if industry can eliminate the 830 million metric tons of carbon dioxide generated every year to make hydrogen, mostly from the steam reformation of methane.

Carbon sequestration costs could decline enough to make "blue" hydrogen—hydrogen for which all carbon emissions from production are captured and stored or reused—affordable by 2030, the IEA says. And only after 2030 could the cost of renewable energy–powered water electrolysis allow "green" hydrogen—hydrogen produced without carbon emissions—to reach affordable prices.

A pollution-free route to water electrolysis is the key to green H2.

Source: International Energy Agency.

• Mexican economic growth has slowed, partly in reaction to the policies of new president Andrés Manuel López Obrador.

• The president's initiatives include a massive refinery in his home state.

• Additional spending by the state oil company, Pemex, may benefit Mexico's chemical industry.

In December 2018, the populist Andrés Manuel López Obrador was sworn in as Mexico's president, becoming the country's first left-of-center leader in nearly 20 years.

Right away, López Obrador made big, controversial decisions. He suspended private energy auctions that previous administrations hoped would resuscitate oil and gas exploration, which was slumping under state oil company Petróleos Mexicanos (Pemex). The president also canceled plans for a new, $13 billion airport for Mexico City.

According to a report issued last year by the consulting firm Deloitte, such decisions resulted in "lower investment and diminished business confidence." Add uncertainty over trade and the economy in general, and the country's outlook has dimmed.

Banco de México revised its economic forecast downward. The central bank initially expected gross domestic product (GDP) to grow between 0.2 and 0.7% in 2019. It finished the year anticipating a decline of 0.2%. For 2020, the bank expects GDP to improve a tepid 0.8–1.8%.

López Obrador is putting a lot of attention on Pemex. Although the firm's refineries are operating at only 40% of capacity, the president is pushing for the construction of an $8 billion refinery in his home state of Tabasco.

Felipe Perez, director of Americas refining and marketing researchat IHS Markit, says Pemex is behind on investments in its existing refineries. The country also faces competition from large, efficient refineries on the US Gulf Coast. "If you are going to put a new refinery in Mexico, the question is, 'Within the strategy for the country, can it be competitive?' " he says.

For Mexico's petrochemical sector, the biggest question is feedstock supply. Braskem Idesa started up an ethylene and polyethylene complex in 2016. But because Pemex isn't providing enough ethane, the plant is running at only 75% of capacity. Braskem Idesa aims to begin construction later this year on a terminal to import the feedstock from the US.

When Pemex does get around to significantly boosting refining output, the chemical industry should benefit from the refining coproducts, says Rina Quijada, vice president for Latin American business development at IHS Markit. "One of the first products that might benefit positively is propylene," she says.

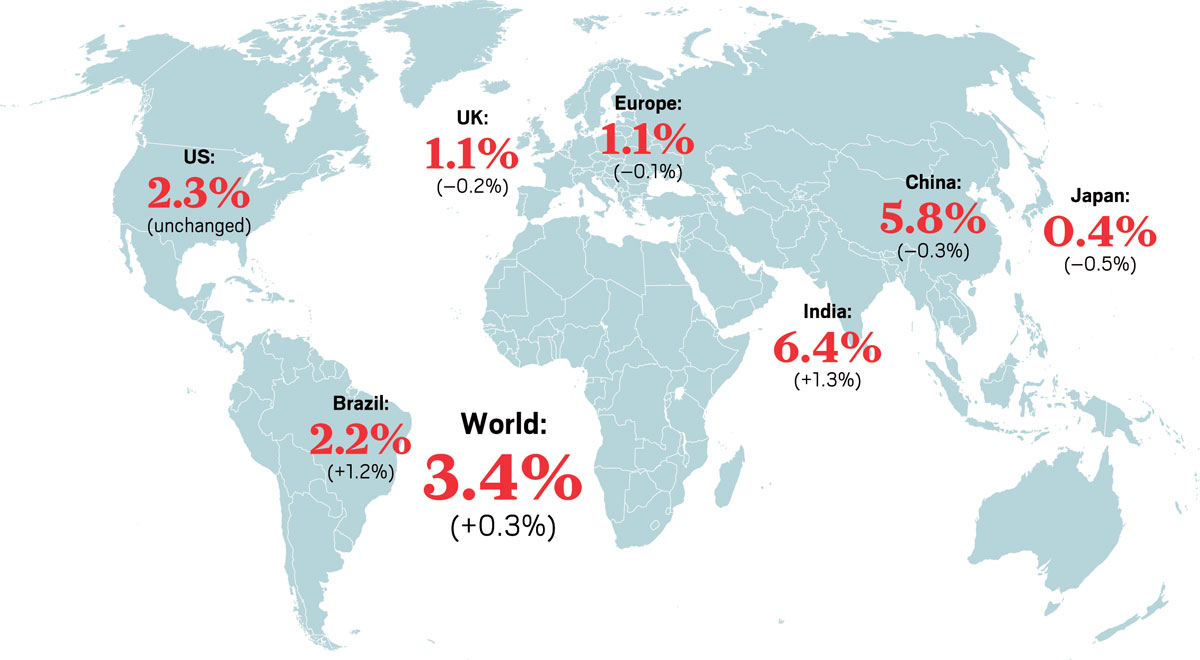

Growth in the global economy decelerated sharply in 2019 as a result of unexpected slowdowns in countries such as Germany, Brazil, and India, according to researchers at the investment bank Goldman Sachs. Ever the optimists, the researchers are calling for increased growth this year, despite slowing in continental Europe, the UK, China, and Japan.

Source: Goldman Sachs. Note: GDP means gross domestic product. Numbers in parentheses are the changes from forecasts for 2019.

World

(+0.3%)

India

(+1.3%)

China

(-0.3%)

US

(unchanged)

Brazil

(+1.2%)

Europe

(-0.1%)

UK

(-0.2%)

Japan

(-0.5%)

Source: Goldman Sachs. Note: GDP means gross domestic product. Numbers in parentheses are the changes from forecasts for 2019.

Already have an ACS ID? Log in

Join the conversation

Contact the reporter

Submit a Letter to the Editor for publication

Engage with us on Twitter