Advertisement

Grab your lab coat. Let's get started

Welcome!

Welcome!

Create an account below to get 6 C&EN articles per month, receive newsletters and more - all free.

It seems this is your first time logging in online. Please enter the following information to continue.

As an ACS member you automatically get access to this site. All we need is few more details to create your reading experience.

Not you? Sign in with a different account.

Not you? Sign in with a different account.

ERROR 1

ERROR 1

ERROR 2

ERROR 2

ERROR 2

ERROR 2

ERROR 2

Password and Confirm password must match.

If you have an ACS member number, please enter it here so we can link this account to your membership. (optional)

ERROR 2

ACS values your privacy. By submitting your information, you are gaining access to C&EN and subscribing to our weekly newsletter. We use the information you provide to make your reading experience better, and we will never sell your data to third party members.

Pharmaceuticals

The year in new drugs

Opinions differ on whether a drop in approvals in 2016 was an anomaly or a worrisome sign about the health of the industry

by Lisa M. Jarvis

January 30, 2017

| A version of this story appeared in

Volume 95, Issue 5

After two years of an open spigot, the flow of new drugs tapered off in 2016. Just 22 new molecular entities were approved in the U.S. last year—less than half the number given the green light in 2015. Industry watchers are left puzzling over how to interpret the drop: as a bad omen for innovation or simply a blip in an otherwise upward trend in productivity?

Some of the dip can be explained by timing and technical glitches. In late 2015, the Food & Drug Administration granted approval to five drugs that industry watchers had expected to be approved in 2016, pushing up the numbers for 2015.

And last year FDA delayed the approval of several medicines—including Sanofi and Regeneron’s arthritis treatment sarilumab and AstraZeneca’s hyperkalemia drug ZS-9—until companies got their plants in compliance with the agency’s current Good Manufacturing Practices (cGMP) standards.

In brief

After two bountiful years, the pharmaceutical industry experienced a sharp drop in new drug approvals in 2016. The decline, to 22 from 45 in 2015, has many drug industry veterans wondering about the health of the sector. Of particular concern was the weakness in oncology approvals, a therapeutic area that in the prior five years was highly productive. But industry experts believe cancer innovation will roar back in 2017. Most expect new drug approvals to return to their recent averages of about 30 medicines a year.

“2016 may serve as a reminder to sponsors that all of their manufacturing facilities must be in compliance with cGMP regulations if they wish to ensure approval of their application,” John Jenkins, FDA’s director of the office of new drugs at the time, said in a blog post reviewing the agency’s performance for the year.

Had all the accelerated or delayed products reached the market in 2016, the number of new drugs might have matched; or at least neared, the average of 30 annual approvals seen over the past decade.

But no amount of number parsing can fix what some see as an inherently weak drug pipeline. Bernard Munos, founder of the InnoThink Center for Research in Biomedical Innovation, notes that seven big pharma companies that collectively won 14 drug approvals in 2015 did not manage to get a single product to market last year.

The seven left empty handed were Amgen, AstraZeneca, Bayer, Bristol-Myers Squibb, GlaxoSmithKline, Johnson & Johnson, and Novartis. Pfizer chalked up one approval, for the eczema treatment Eucrisa, only because it paid $5.2 billion for Anacor, which had already filed a new drug application for the treatment at the time of the deal.

Eli Lilly & Co., Merck & Co., Biogen, and AbbVie were the only big pharma companies to add more than a single drug to their portfolio; each firm had two approvals in 2016.

Big pharma’s approval dearth in 2016 “is a reflection of the inherent softness in the pipeline,” Munos says, adding that the situation “doesn’t bode well” for the sustainability of the industry.

Pipeline potholes

Many companies experienced unexpected setbacks to advanced drug candidates in 2016

May 27: AstraZeneca says FDA turned down a new drug application for its hyperkalemia treatment ZS-9 due to manufacturing issues.

June 7: Biogen’s multiple sclerosis drug opicinumab fails a Phase II trial, but the company appears to be continuing to develop it.

June 14: Infinity Pharmaceuticals’ PI3K inhibitor duvelisib fails a Phase II study as a non-Hodgkin lymphoma treatment, prompting AbbVie to drop a partnership and Infinity to announce layoffs.

July 7: Juno Therapeutics says FDA put on hold a clinical trial of its CAR T-cell therapy JCAR015 after deaths of patients with cancer. The hold was subsequently lifted and then reinstated in November after more deaths.

Sept. 21: Gilead Sciences ends a Phase II/III study of GS-5745, an anti-MMP9 antibody for ulcerative colitis, due to lack of efficacy. Studies in gastric cancer and other diseases continue.

Oct. 5: Alnylam ends development of the RNAi-based therapy revusiran, in Phase III studies for hereditary amyloidosis with cardiomyopathy, after patient deaths during a trial.

Nov. 1: Pfizer ends development of its PCSK9 inhibitor bococizumab, which had been in two Phase III studies, out of concern that it could not effectively compete in the lipid-lowering market.

Nov. 23: Eli Lilly & Co.’s anti-amyloid treatment solanezumab fails its third Phase III study as an Alzheimer’s disease treatment.

Nov. 29: Arrowhead Pharmaceuticals ends development of three drug candidates, including a hepatitis B treatment in Phase II trials, based on worries about the safety of its RNAi delivery system.

Dec. 12: Ophthotech’s wet age-related macular degeneration treatment Fovista fails two Phase III trials, prompting the firm to cut 80% of its staff.

Dec.29: Cempra’s antibiotic solithromycin is turned back by FDA, which suggests that a trial of 9,000 people should be run to assess the drug’s safety.

Source: Companies, FDA

To sustain a $20 billion-a-year business, a firm needs to add one new blockbuster drug to its portfolio each year, Munos points out. For big pharma firms with much higher sales, four such $1 billion-per-year drugs are needed to maintain their revenue base. “Nobody is at that level,” he adds.

Indeed, between 2012 and 2016, none of the major companies managed to average more than two approvals per year, according to data from the health care investing firm HBM Partners. Roche and Merck came the closest, with eight new products in that time frame, though the six new treatments Gilead Sciences added to its portfolio have much greater commercial potential than anyone else’s innovative drugs.

One of the most notable shifts in 2016 was the drop in cancer drug approvals. Over the past decade, oncology has eclipsed all other therapeutic areas in the number of new drugs to reach the market; 50 cancer treatments were approved between 2012 and 2016, and it has drawn deep investment from big pharma firms. But in 2016, just four new cancer treatments were approved—a far cry from the 14 okayed in 2015.

Views differ on how to interpret the paucity of cancer drugs in 2016. Two of the five drugs FDA pushed through at the end of 2015 were for cancer.

The two were also among a number of new products, including five cancer treatments, approved in 2015 that FDA called “breakthrough therapies,” a status granted to molecules that are highly innovative or address underserved diseases. Developers of such drugs get extra guidance from the agency, an all-hands-on-deck approach that trimmed clinical development times and may have gotten them on the market sooner.

And scientific innovation caused bursts of activity for certain indications that could be hard to match going forward. In 2015, points out Hardik Patel, oncology analyst at the health care consulting firm Datamonitor, eight drugs were approved for two types of cancer—lung and multiple myeloma.

“Although these are two of the largest oncology indications, I think this kind of production is difficult to sustain year-on-year,” he says.

Drop

Moreover, the oncology field is watching for several key approvals this year. “I think we’re in a lull right now waiting for several major readouts that are expected to hit during 2017, so I’m not particularly worried about the drop-off,” says Sally Church, editor of Biotech Strategy Blog, which focuses on cancer drug development.

Datamonitor projects 10 oncology treatments will be approved this year, including three for acute myeloid leukemia, or AML: Celgene’s enasidenib, an IDH2 inhibitor licensed from Agios; Novartis’s FLT2 inhibitor midostaurin; and Jazz Pharmaceuticals’ Vyxeos, a liposomal formulation of cytarabine and daunorubicin. “The AML market is set to see large growth, as there are currently no approved drugs for the disease in the U.S.,” Patel notes.

Three other drugs on the Datamonitor list are cancer immunotherapies. Two are checkpoint inhibitors—antibodies that take the brakes off the immune system—and the other is the first chimeric antigen receptor T-cell therapy, which is engineered from a patient’s own cells to find and destroy cancer cells.

Many of the oncology deals that big companies signed in recent years were aimed at building up a portfolio of cancer immunotherapies, and digestion of those drug development programs is another reason cited for the 2016 slowdown. Companies with checkpoint inhibitors have accumulated an array of complementary molecules and are now trying to figure out which combinations will improve the effectiveness of cancer immunotherapy.

Meager crop

New drug approvals in the U.S. fell by more than half in 2016 compared to the prior year

Spinraza (oligonucleotide)

Active Ingredient: Nusinersen

Applicant: Biogen/Ionis

Indication: Spinal muscular atrophy

Mode of action: SMN2 directed antisense

FDA special status: Fast track | Orphan drug | Novel mode of action | Priority review

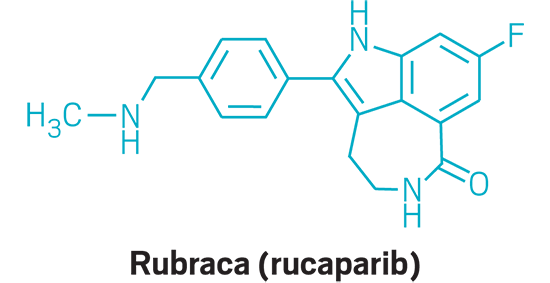

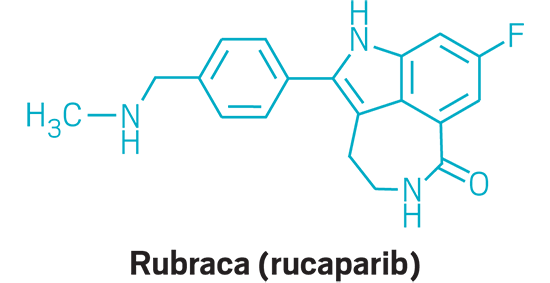

Rubraca (small molecule)

Active Ingredient: Rucaparib

Applicant: Clovis Oncology

Indication: BRCA-positive ovarian cancer

Mode of action: PARP inhibitor

FDA special status: Orphan drug | Breakthrough drug | Priority review | Accelerated approval

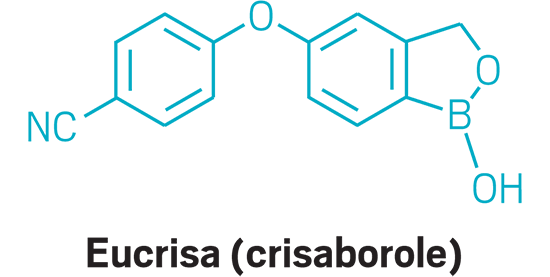

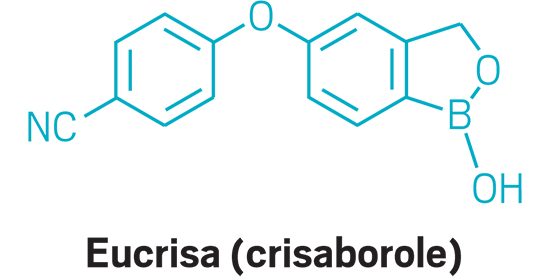

Eucrisa (small molecule)

Active Ingredient: Crisaborole

Applicant: Pfizer

Indication: Eczema

Mode of action: PDE-4 inhibitor

Zinplava (antibody)

Active Ingredient: Bezlotoxumab

Applicant: Merck & Co.

Mode of action: Clostridium difficile infection

Indication: Neutralization of Clostridium difficile toxin B

FDA special status: Fast track | Priority review | Novel mode of action

Lartruvo (antibody)

Active Ingredient: Olaratumab

Applicant: Eli Lilly & Co

Indication: Soft tissue sarcoma

Mode of action: PDGF-alpha inhibitor

FDA special status: Fast track | Orphan drug | Breakthrough drug | Priority review | Accelerated approval

Exondys 51 (oligonucleotide)

Active Ingredient: Eteplirsen

Applicant: Sarepta

Indication: Duchenne muscular dystrophy

Mode of action: Exon-skipping to enable production of dystrophin

FDA special status: Fast track | Orphan drug | Priority review | Novel mode of action | Accelerated approval

Adlyxin (peptide)

Active Ingredient: Lixisenatide

Applicant: Sanofi

Indication: Type-2 diabetes

Mode of action: GLP-1 agonist

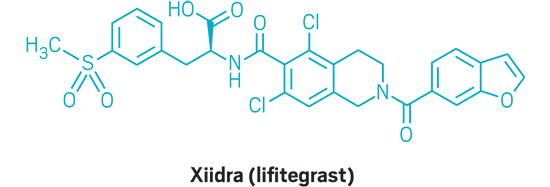

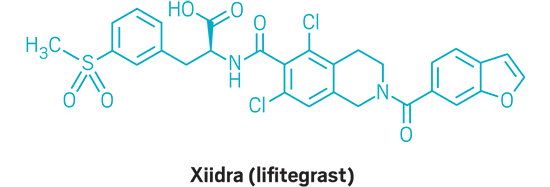

Xiidra (small molecule)

Active Ingredient: Lifitegrast

Applicant: Shire

Indication: Dry eye

Mode of action: LFA-1 antagonist

FDA special status: Priority review | Novel mode of action

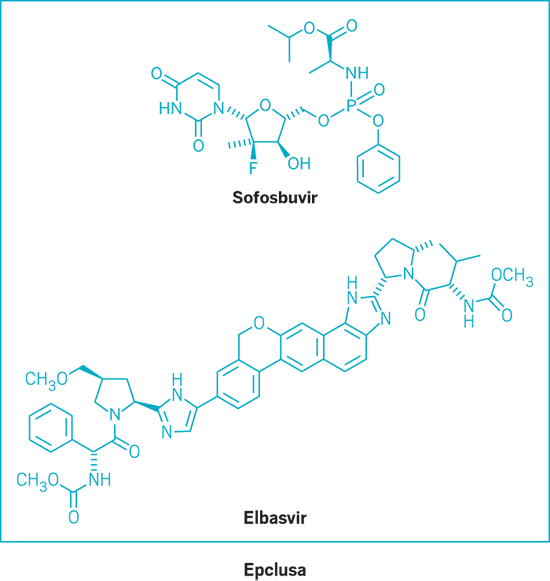

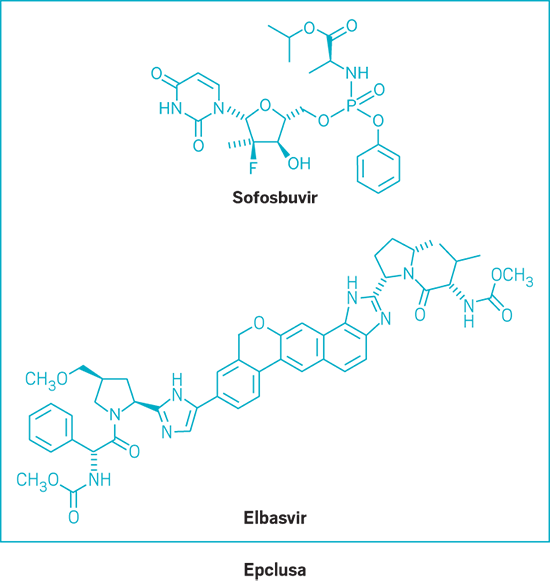

Epclusa (small molecule)

Active Ingredient: Sofosbuvir and velpatasvir

Applicant: Gilead Sciences

Indication: HCV, all genotypes

Mode of action: NS5B polymerase and NS5A inhibitors

FDA special status: Fast track | Breakthrough drug | Priority review

Netspot (small molecule)

Active Ingredient: Gallium Ga 68 dotatate

Applicant: Advanced Accelerator Applications USA

Indication: PET imaging agent

Mode of action: Radioactive diagnostic

FDA special status: Orphan drug | Priority review

Axumin (small molecule)

Active Ingredient: Fluciclovine F 18

Applicant: Blue Earth Diagnostics

Indication: PET imaging agent

Mode of action: Radioactive diagnostic

FDA special status: Priority review

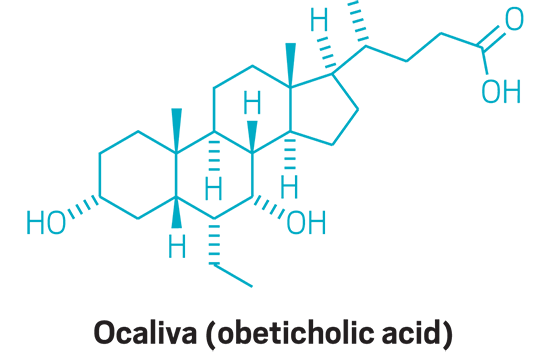

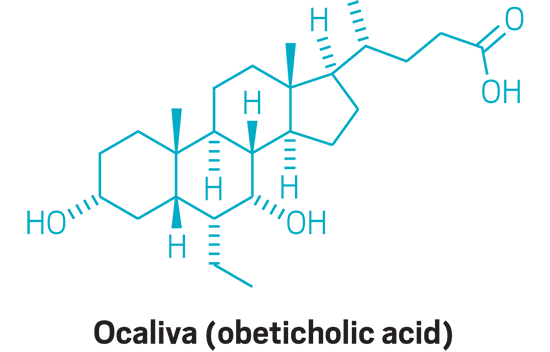

Ocaliva (small molecule)

Active Ingredient: Obeticholic acid

Applicant: Intercept Pharmaceuticals

Indication: Primary biliary cholangitis

Mode of action: FXR inhibitor

FDA special status: Fast track | Orphan Drug | Priority review | Accelerated approval | Novel mode of action

Zinbryta (antibody)

Active Ingredient: Daclizumab

Applicant: Biogen/AbbVie

Indication: Multiple sclerosis

Mode of action: IL-2 receptor antagonist

FDA special status: Novel mode of action

Tecentriq (antibody)

Active Ingredient: Atezolizumab

Applicant: Roche/Genentech

Indication: Bladder cancer

Mode of action: PD-L1 inhibitor

FDA special status: Breakthrough drug | Priority review | Accelerated approval

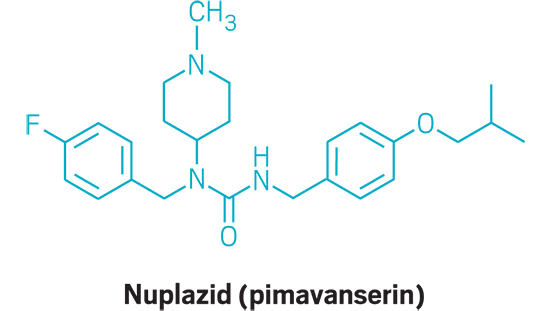

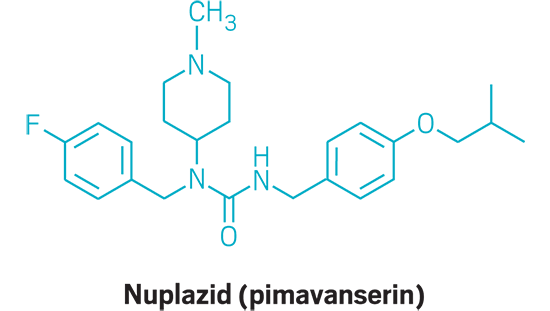

Nuplazid (small molecule)

Active Ingredient: Pimavanserin

Applicant: Acadia Pharmaceuticals

Indication: Psychosis associated with Parkinson’s disease

Mode of action: Serotonin 5-HT2a receptor agonist

FDA special status: Breakthrough drug | Priority review

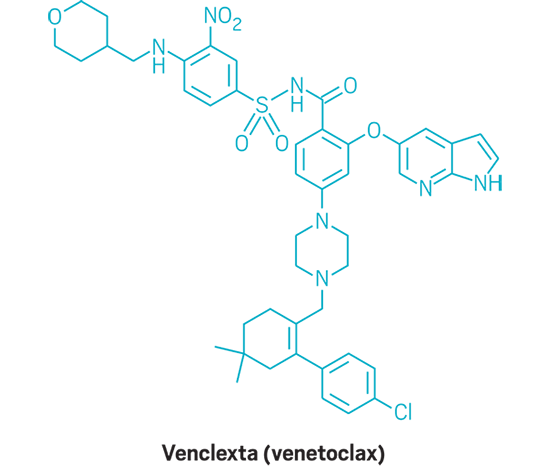

Venclexta (small molecule)

Active Ingredient: Venetoclax

Applicant: AbbVie

Indication: Chronic lymphocytic leukemia

Mode of action: BCL-2 inhibitor

FDA special status: Orphan drug | Breakthrough drug | Priority review | Novel mode of action | Accelerated approval

Defitelio (oligonucleotide)

Active Ingredient: Defibrotide sodium

Applicant: Jazz Pharmaceuticals

Indication: Severe hepatic veno-occlusive disease

Mode of action: Unknown

FDA special status: Fast track | Orphan drug | Priority review | Novel mode of action

Cinqair (antibody)

Active Ingredient: Reslizumab

Applicant: Teva Pharmaceuticals

Indication: Asthma

Mode of action: IL-5 inhibitor

Taltz (antibody)

Active Ingredient: Ixekizumab

Applicant: Eli Lilly & Co.

Indication: Mode of action: Psoriasis

Mode of action:: IL-17A inhibitor

Anthim (antibody)

Active Ingredient: Obiltoxaximab

Applicant: Elusys Therapeutics

Indication: Anthrax treatment

Mode of action: B. anthracis toxin neutralizer

FDA special status: Fast track | Orphan drug

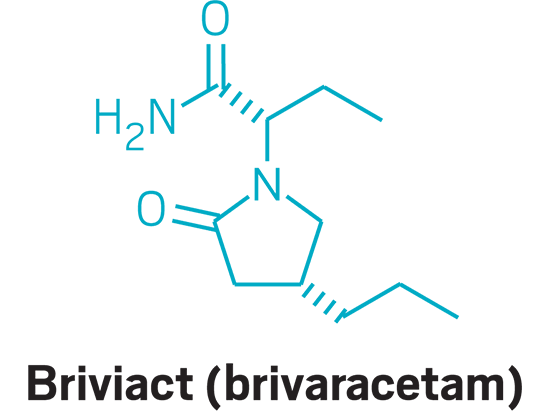

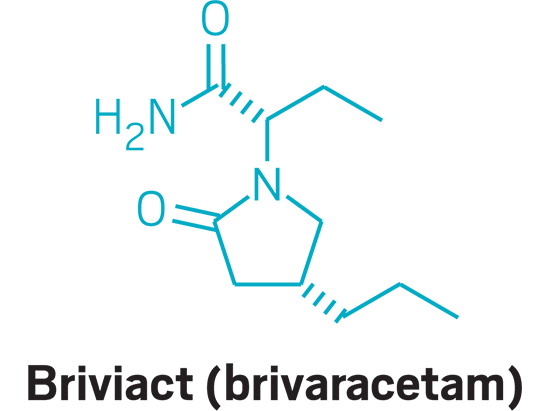

Briviact (small molecule)

Active Ingredient: Brivaracetam

Applicant: UCB

Indication: Epilepsy

Mode of action:: Unknown

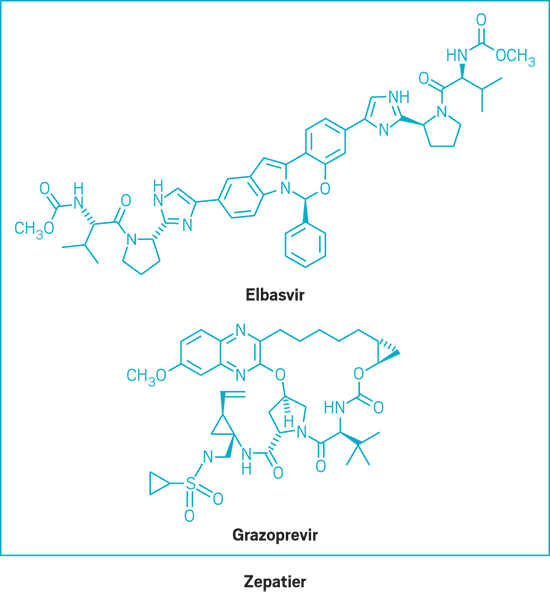

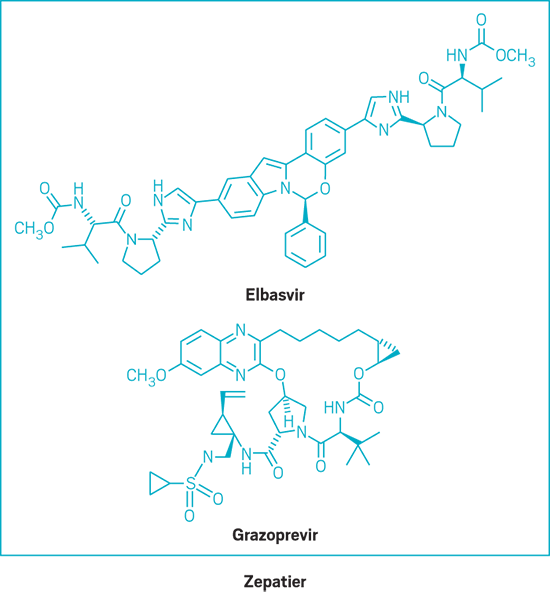

Zepatier (small molecule)

Active Ingredient: Elbasvir and grazoprevir

Applicant: Merck & Co.

Indication: HCV genotypes 1 & 4

Mode of action: NS5A inhibitor and NS3/4A protease inhibitor

FDA special status: Priority review | Breakthrough drug

Key

Small Molecule

Oligonucleotide

Peptide

Antibody

FDA fast track

Orphan drug

FDA breakthrough status

FDA priority review

Novel mode of action

FDA accelerated approval

FDA priority review voucher earned

Drugs with viewable structures

| DRUG NAME | ACTIVE INGREDIENT | APPLICANT | MODE OF ACTION | INDICATION |

|---|---|---|---|---|

| Spinraza | Nusinersen | Biogen/Ionis | Exon-skipping to enable production of SMN protein | Spinal muscular atrophy |

| Rubraca | Rucaparib | Clovis Oncology | PARP inhibitor | BRCA-positive ovarian cancer |

| Eucrisa | Crisaborole | Pfizer | PDE-4 inhibitor | Eczema |

| Zinplava | Bezlotoxumab | Merck & Co. | Neutralization of Clostridium difficile toxin B | Clostridium difficile infection |

| Lartruvo | Olaratumab | Eli Lilly & Co | PDGF-α inhibitor | Soft tissue sarcoma |

| Exondys 51 | Eteplirsen | Sarepta | Exon-skipping to enable production of dystrophin | Duchenne muscular dystrophy |

| Adlyxin | Lixisenatide | Sanofi | GLP-1 agonist | Type-2 diabetes |

| Xiidra | Lifitegrast | Shire | LFA-1 antagonist | Dry eye |

| Epclusa | Sofosbuvir and velpatasvir | Gilead Sciences | NS5B polymerase and NS5A inhibitors | HCV, all genotypes |

| Netspot | Gallium Ga 68 dotatate | Advanced Accelerator Applications USA | Radioactive diagnostic | PET imaging agent |

| Axumin | Fluciclovine F 18 | Blue Earth Diagnostics | Radioactive diagnostic | PET imaging agent |

| Ocaliva | Obeticholic acid | Intercept Pharmaceuticals | FXR inhibitor | Primary biliary cholangitis |

| Zinbryta | Daclizumab | Biogen/AbbVie | IL-2 receptor antagonist | Multiple sclerosis |

| Tecentriq | Atezolizumab | Roche/Genentech | PD-L1 inhibitor | Bladder cancer |

| Nuplazid | Pimavanserin | Acadia Pharmaceuticals | Serotonin 5-HT2a receptor agonist | Psychosis associated with Parkinson's disease |

| Venclexta | Venetoclax | AbbVie | BCL-2 inhibitor | Chronic lymphocytic leukemia |

| Defitelio | Defibrotide sodium | Jazz Pharmaceuticals | Unknown | Severe hepatic veno-occlusive disease |

| Cinqair | Reslizumab | Teva Pharmaceuticals | IL-5 inhibitor | Asthma |

| Taltz | Ixekizumab | Eli Lilly & Co. | IL-17A inhibitor | Psoriasis |

| Anthim | Obiltoxaximab | Elusys Therapeutics | B. anthracis toxin neutralizer | Anthrax treatment |

| Briviact | Brivaracetam | UCB | Unknown | Epilepsy |

| Zepatier | Elbasvir and grazoprevir | Merck & Co. | NS5A inhibitor and NS3/4A protease inhibitor | HCV genotypes 1 & 4 |

To download a pdf of this article, visit http://cenm.ag/newdrugs16.

“The focus has definitely shifted to combinations to boost responses, and those take time” to develop, Church says. Market watchers could get some hints about effective combinations at cancer conferences this year.

Although cancer drug approvals should bounce back in 2017, the numbers mask a productivity problem. The pipeline is packed with new treatments, but a smaller percentage is actually getting past FDA and reaching patients. Meanwhile, the cost of getting those drugs to market is increasing, Munos says.

“The clinical success rate in oncology, in spite of everything that we’ve seen, keeps dropping,” he says. “That is not what you’d expect from a therapeutic area where you have a successful wave of innovation happening.”

2016 new drug approvals by the numbers

22: New molecular entities approved in 2016

45: Approved in 2015

8: Drugs with a novel mechanism of action approved

14: Cancer drugs approved in 2015

50%: Small molecules approved

4: Cancer drugs approved in 2016

$750,000: Price of first year of treatment of Biogen’s Spinraza

2: Antisense treatments approved

Source: FDA, companies

Beyond oncology, the industry experienced several major setbacks to the drug pipeline in 2016. In many cases, the failed drug candidates had been tested in thousands of patients, representing many years of research and investment.

The most notable case came late in the year, when Lilly said its anti-amyloid antibody solanezumab, for Alzheimer’s disease, failed a third Phase III study. Although investor expectations for the trial were low, the lack of efficacy was a disappointment for the Alzheimer’s community, which currently lacks any treatments that can slow down the disease. Solanezumab is the third Alzheimer’s drug disappointment to come from Lilly’s pipeline; the γ-secretase inhibitor semagacestat and the BACE inhibitor LY2886721 failed in 2010 and 2013, respectively.

Pfizer, meanwhile, halted development of its PCSK9 inhibitor, bococizumab. The big pharma firm said it was ending work on the antibody because it simply wouldn’t be competitive in the lipid-lowering arena, in which two PCSK9 inhibitors are already on the market.

And although nucleic acid developers had victories in 2016 with the approval of two antisense oligonucleotides—Biogen and Ionis Pharmaceuticals’ spinal muscular atrophy treatment Spinraza and Sarepta Therapeutics’ Duchenne muscular dystrophy treatment Exondys 51—they also had significant setbacks.

Alnylam scuttled development of its most advanced RNAi-based therapy, revusiran, after seeing unwanted side effects and some patient deaths during a Phase III study in hereditary ATTR amyloidosis. And in November Arrowhead Pharmaceuticals jettisoned three of its RNAi programs over concerns about the safety of its delivery technology.

Although 2017 brings a clean slate, and forecasts suggest the industry will at least return to its recent average of 30 approvals per year, Munos is quick to point out that problems abound. “The numbers may be better this year,” he says, “but the industry is still going to face headwinds.”

To download a pdf of this article, visit http://cenm.ag/newdrugs16.

You might also like...

The power is now in your (nitrile gloved) hands

Sign up for a free account to get more articles. Or choose the ACS option that’s right for you.

Already have an ACS ID? Log in

Join the conversation

Contact the reporter

Submit a Letter to the Editor for publication

Engage with us on Twitter