Advertisement

Grab your lab coat. Let's get started

Welcome!

Welcome!

Create an account below to get 6 C&EN articles per month, receive newsletters and more - all free.

It seems this is your first time logging in online. Please enter the following information to continue.

As an ACS member you automatically get access to this site. All we need is few more details to create your reading experience.

Not you? Sign in with a different account.

Not you? Sign in with a different account.

ERROR 1

ERROR 1

ERROR 2

ERROR 2

ERROR 2

ERROR 2

ERROR 2

Password and Confirm password must match.

If you have an ACS member number, please enter it here so we can link this account to your membership. (optional)

ERROR 2

ACS values your privacy. By submitting your information, you are gaining access to C&EN and subscribing to our weekly newsletter. We use the information you provide to make your reading experience better, and we will never sell your data to third party members.

Biosimilars

Biobetters May Be A Better Bet

Improving on biologic drugs is an alternative to taking a more generic route

by Ann M. Thayer

March 25, 2013

| A version of this story appeared in

Volume 91, Issue 12

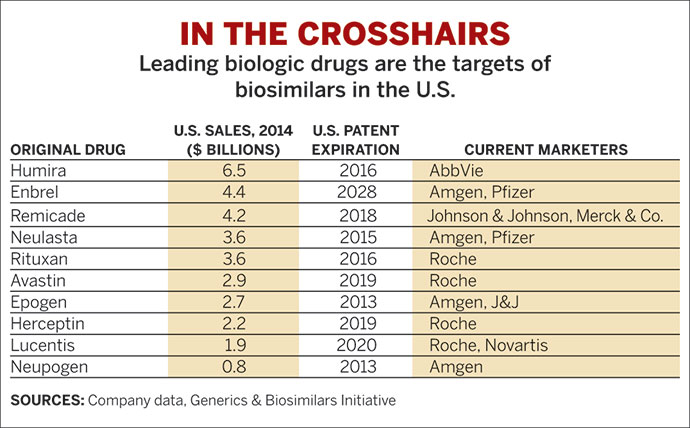

Prospects for developers of biosimilars, near copies of off-patent biologic drugs, look outstanding on paper. By the end of the decade, patents will have expired on at least 20 blockbuster biologic drugs that together have annual sales of more than $50 billion. Europe, with biosimilars regulations on the books since 2005, has already approved several products, and many other countries are following suit.

But so far, biosimilars are just a tiny fraction of the $160 billion-per-year biologics market. By 2016 they will still be worth only about $5 billion in an even larger biologics business, according to the market research firm IMS Health. It turns out that getting biosimilars to market is harder than expected, especially in the U.S. As a result, some companies are turning their attention instead to a class of improved biologic drugs known as biobetters.

In February 2012, U.S. regulators finally issued long-awaited draft guidelines for developers of biosimilar drugs. While the guidelines answer some questions, they also leave many aspects of the process to be determined on a case-by-case basis.

To be approved, a biosimilar must be shown to be as exact a copy as possible of an existing biologic—an untested process in the U.S. that may prove problematic because the criteria for demonstrating exactness are not yet well defined. The U.S. guidance also isn’t clear on whether, like small-molecule generic drugs, biosimilars can be prescribed interchangeably with an approved product.

Lingering regulatory uncertainties, along with technical and commercial challenges, have made some developers rethink their strategy. For example, Israel’s Teva Pharmaceutical Industries and its manufacturing partner Lonza, as well as South Korea’s Samsung BioLogics, were reported in late 2012 to have paused clinical development of versions of rituximab, a Roche monoclonal antibody used to treat cancer and rheumatoid arthritis. Sales of the patented drug last year were $7 billion.

Roche had been bracing for rituximab competitors to emerge this year when patents expire in Europe, but the company now expects to have the market to itself until about 2016, Chief Executive Officer Severin Schwan told analysts in January during a conference call.

A year ago, Pfizer and India’s Biocon parted ways as biosimilars business partners, claiming their priorities diverged. In 2010, Pfizer had paid Biocon $200 million for rights to four insulin-related products. Last month, Biocon joined instead with the generic drug firm Mylan to develop versions of insulin analogs.

Meanwhile, Merck & Co., which launched a biosimilars business in 2009 to great fanfare, appears to have pulled back. Last year it folded the venture into its development operations “to facilitate decision making and prioritization of resources,” according to a company spokesman. Merck also halted a multi-million-dollar agreement dating from 2011 to license a biosimilar form of Amgen’s arthritis treatment Enbrel from South Korea’s Hanwha Chemical.

Changing course again, last month Merck transferred multiple biosimilar candidates to Samsung Bioepis, a joint venture between Samsung and Biogen Idec. Merck’s new partner will take over development, manufacturing, and approval, leaving it with only commercialization. The deal lets Merck “advance several biosimilars while pursuing an internal biologics pipeline that includes novel, biobetter, and biosimilar programs,” the spokesman adds.

For established biopharmaceutical firms, the class of biologic drugs being called biobetters, or biosuperiors, may offer better opportunities and fewer pitfalls than biosimilars. “That’s where the higher prices and higher margins will be,” says R. Stephen Porter, chief science officer of Hong Kong-based Dragon Bio-Consultants.

A biobetter is a related or improved version of a drug—marketed or a candidate that is or has been in development—with properties that will allow it to compete on more than price with older products. Many biobetters boast new, easier-to-administer forms or longer half-lives in the body, Porter says. Biobetters may also find use in different or broader patient groups. In contrast, biosimilars offer no clinical advantage compared with the original drug and may be surpassed by second-generation products.

Unlike everyday small-molecule generic drugs, biosimilars and biobetters are expensive to develop. Sandoz, the generic drug arm of Novartis, estimates that it takes seven to eight years and up to $250 million to make a complex biologic drug and then prove its similarity to the original in quality, structure, and therapeutic effect. Biobetters will take longer and cost even more, but they are expected to warrant patent protection and premium prices, rather than sell at a discount like biosimilars.

MedImmune, the biologics arm of AstraZeneca, has launched a biobetters effort. “The three pillars of our biosuperiors program are efficacy, safety, and convenience,” says Steve Coats, senior director for chemistry. Applying protein engineering and other technologies to manipulate proteins and antibodies “will allow us to truly differentiate from an existing molecule,” he adds. MedImmune’s biosuperiors are directed at targets validated in at least a Phase IIb clinical study through to registration trials and product launches.

Regulators treat biobetters as new molecules that must follow the full drug approval pathway, Coats points out. Even so, going into the clinic against a validated target may allow for some streamlining of the development process because of preexisting clinical data. And the odds are better that the drug will work. “The ability to develop a therapy against a clinically validated target should reduce the clinical risk,” he adds.

Although many companies are trying to develop biosimilars and biobetters, those most likely to succeed are experienced biologics firms that have technology, manufacturing, clinical, and regulatory expertise, industry participants suggest. These companies are already beefing up versions of their own and each others’ products, such as Roche with new delivery methods for its rituximab, and using more modern second-generation manufacturing methods. For example, Amgen, which is working with the generic drug firm Actavis, uses the slogan “Manufacturing matters” as part of its biosimilars efforts.

Manufacturing presents one of the biggest obstacles for developers of biosimilars and biobetters, because small differences in the cell line, production methods, and purification steps can alter the final protein structure as well as its activity and safety. As a result, regulators have been asking originator companies to provide biosimilar developers with details on manufacturing from their approved drug filings, which they are loath to share, to help determine the similarity of follow-on products.

Despite the barriers to entry, the biosimilars field is attracting many new entrants, according to Deborah Slagle, vice president for marketing and R&D at SAFC, Sigma-Aldrich’s fine chemicals division and a supplier of cell lines, cell-culture media, and other products to biologics manufacturers. The firm has seen an increase in customer interest for biomanufacturing technologies and products that can support cost-effective production. “We are seeing a tremendous amount of uptake with our customers in the Asia-Pacific region,” she says, many of which are Asian companies developing biosimilars for local markets.

Dragon Bio-Consultants’ Porter believes “there are going to be some shakeouts” as production quality improves and low-cost Asian competition emerges. But for now, biosimilars may likely serve less-regulated emerging markets while higher-priced biobetters find places on Western shelves.

You might also like...

The power is now in your (nitrile gloved) hands

Sign up for a free account to get more articles. Or choose the ACS option that’s right for you.

Already have an ACS ID? Log in

Join the conversation

Contact the reporter

Submit a Letter to the Editor for publication

Engage with us on Twitter