If you have an ACS member number, please enter it here so we can link this account to your membership. (optional)

ERROR 2

ACS values your privacy. By submitting your information, you are gaining access to C&EN and subscribing to our weekly newsletter. We use the information you provide to make your reading experience better, and we will never sell your data to third party members.

Economic health across the globe should mean a good 2018 for the world chemical industry

Even when the economic times are good, one region of the globe typically lags. Perhaps Japan is in recession, or Latin America is racked by turmoil, or Europe is struggling with slow growth. But as the calendar flips to 2018, the view is fine pretty much all around. The arrows are pointing up for every economically important country, and the consulting firm PwC predicts that the global economy overall will expand by almost 4%, the fastest rate since 2011. With just a couple exceptions, outlooks for key chemical markets are equally bright. Yes, economies can turn on a dime, but at the moment, 2018 looks to be a very good year for the global chemical enterprise.

Advertisement

Electronic materials

Semiconductors are humming, but displays are heading for a fall

This immersion scanner, made by ASML, is used in multiple patterning, one of several advanced photolithography methods driving demand for semiconductor materials.

The good times will likely keep on rolling for suppliers of semiconductor materials in 2018, at least in the first half. But the display materials market, prone to rapid boom-bust cycles, appears to be heading downward.

“Since demand for DRAM and NAND memory chips remains strong, the first half of 2018 will be good,” says Keiji Mihayashi, president of Fujifilm Electronic Materials, which supplies both the semiconductor and display industries. Strong demand for the two types of memory chip is linked to cloud computing, he adds.

Memory chips are a major market for firms like Fujifilm, Mihayashi notes. “High demand for the chips will boost the results of memory manufacturers, and sales of materials will correspondingly be good as well.” It’s too early to tell what the second half of 2018 will bring, he says.

Lita Shon-Roy, president of the electronic materials consulting firm Techcet, points to other reasons the semiconductor materials market is buoyant. Newly built semiconductor plants in China are boosting demand for materials. And advanced chips are often made using a materials-intensive manufacturing technique called multiple patterning. Meanwhile, supplies of materials remain tight across the semiconductor industry because “producers don’t expand capacity just because of one or two good years,” Shon-Roy says.

Silicon wafers are in the shortest supply because only a few firms make them. Supplies of high-purity gases and wet chemicals are limited as well. Any unexpected production halt can stress the supply chain, she notes.

The picture isn’t so bright for manufacturers of materials used in TVs and other flat-panel displays. The display market is prone to periods of oversupply when large, new plants come on-line, and this is happening now.

“A supply glut is widely expected, which will lead to a decline in panel prices,” warns Sang-Ho Kang, display technologies global business director at DowDuPont. “Display materials markets will feel growing price pressure from panel makers.”

But newer display technologies will spur both consumer demand and the need for new materials, Kang adds. For instance, the market for organic light-emitting diode displays is small but growing rapidly. And DowDuPont researchers are developing materials for use in foldable displays, which Kang expects to hit the market this year.

After years of planning and construction, Enerkem's plant began producing bioethanol in September.

The worldwide fight against climate change took a hit in mid-2017 when the Trump administration pulled the U.S. out of the Paris climate agreement. But the rest of the world—along with 14 states and more than two dozen cities within the U.S.—is moving ahead with policies that put a bull’s-eye on carbon emissions.

In December, China kicked off a cap-and-trade carbon market for its energy industry. The market’s rules have yet to be announced, but China’s need for renewable power will drive a global 20% increase in solar installations this year, the consulting firm IHS Markit predicts.

Meanwhile, the Canadian government is working to impose a carbon tax on provinces that don’t meet its standards for reducing emissions.

In the U.S., the new tax legislation preserved key tax credits for the solar and wind industries, which now produce 7% of the nation’s electricity. As utilities continue to shutter coal-fired power plants, reliance on renewable sources will rise. The growth of renewables has put a new focus on energy storage, including batteries. The storage market will roughly double in size to nearly 600 MW in 2018, according to GTM Research and the Energy Storage Association.

The New York State Energy Research & Development Authority has invested in 50 energy storage technology projects as part of its commitment to supply 50% of the state’s power from renewables by 2030. New York is one of the U.S. states that will uphold the Paris Agreement.

In contrast, the outlook for advanced biofuels has not improved. In the U.S., two of three much-touted cellulosic ethanol facilities—operated separately by DuPont and Abengoa—have been shut down.

A few bright spots persist for the biobased chemicals industry in 2018. Projects to produce jet fuels from waste and from purpose-grown crops have attracted corporate support. Firms such as Enerkem and Fulcrum BioEnergy are successfully producing chemicals and fuels from municipal solid waste.

And some industrial biotechnology companies are reporting strong demand. DuPont’s Sorona fibers, made with biobased propanediol, are now in everything from jeans to high-end fashion, the company says. Its biobased ingredients are increasingly popular with marketers of cleaning and food products.

“We have been accelerating the pace of our new product introductions over the past few years, and in 2018 you will see new products in basically every market space we serve,” says William Feehery, president of DuPont Industrial Biosciences.

Dow Chemical started up this ethylene cracker in Freeport, Texas, last year.

Petrochemical makers in the U.S. are in the midst of commissioning the largest fleet of new ethylene crackers in more than a generation. However, the new supply shouldn’t sink profitability anytime soon.

With little capacity coming onstream elsewhere in the world, significant construction delays, and new plants for derivatives such as polyethylene already running, the world will need every metric ton of ethylene the new crackers will crank out. It won’t be until the middle of 2018 that they begin to ease a tight market.

The global ethylene market is snug, with effective operating rates—the utilization rate of plants that are running—at 92%, according to Steve Lewandowski, vice president of olefins for IHS Markit. “There is no spare capacity anywhere,” he says.

Hurricane Harvey, which made landfall in Texas on Aug. 25, 2017, cut through the heart of the U.S. chemical industry. By Sept. 5, more than half of U.S. ethylene capacity and 36% of ethylene derivative capacity was off-line, according to IHS Markit.

But the region bounced back quickly. Damage to chemical facilities was limited, and all but a few plants were up and running again by the end of the month.

Overall, the industry lost some 750,000 metric tons of ethylene production, nearly a cracker’s worth of output for a year. “That doesn’t sound like much,” Lewandowski says. “But when the whole system is pushing to the maximum operating rate, any disruption is a problem.”

Longer-lasting effects of Harvey are construction delays of about six months for two new crackers, each with 1.5 million metric tons of annual capacity, that ExxonMobil and Chevron Phillips Chemical meant to start up by the end of 2017.

These two companies already turned on new polyethylene plants earlier last year. With these and similar additions, Lewandowski says, the U.S. will have much more capacity for derivatives than for ethylene, straining ethylene supplies until the crackers are completed and up to full production around the middle of 2018.

In addition to the ExxonMobil and Chevron Phillips crackers, Indorama is set to restart a long-idled cracker in Lake Charles, La., and Formosa Plastics is due to complete a new cracker in Point Comfort, Texas, Lewandowski says. Shin-Etsu Chemical and Sasol will likely complete their ethylene projects in 2019.

Bob Patel, CEO of polymer maker LyondellBasell Industries, argues that the market for polyethylene won’t soften much either. He predicts operating rates for that product may remain above 90%.

Speaking to analysts in October, Patel explained that increases in polyethylene production outstripped demand growth by about 3% in 2017 and will by another 1% in 2018. “If you look across those two years, you end up with perhaps operating rates declining by 3% or 4% coming off very, very high operating rates and what we would consider still to be balanced markets,” he said.

Cibus plant researchers examine plant clones that have gene-edited, rather than transgenic, traits.

While the global economy heats up, farmers face yet another year of low commodity prices. After four years of recession for U.S. growers, farm incomes are down about 25% from 2014. Adding insult to injury, corn production remains on track for another record-breaking year.

When commodity prices are low, farmers are more sensitive to prices for the inputs they use. Will they make their money back on pricey new biotech seeds and patented pesticides? And with fewer firms competing for their business thanks to an epic wave of corporate consolidation, concerns about affordability will only rise.

Worries over competition have prompted the European Union to delay its deadline for antitrust review of Monsanto and Bayer’s proposed merger until March.

In November, the antitrust activist group Open Markets Institute pointed out that Monsanto-Bayer would be the world’s largest seller of herbicides and seeds for vegetable and cotton crops. It would be the world’s largest owner of intellectual property for herbicide-tolerant seed traits and the largest company researching seeds and traits. Lastly, it would be a huge player in the rise of agricultural data platforms.

But a lot of research and investment is happening outside giant firms like Monsanto, Bayer, and DowDuPont. Start-ups are largely leading innovations in automation and agricultural biotechnology. For example, Cibus used gene editing to develop a nontransgenic canola crop that is tolerant to sulfonylurea herbicides. The website AgFunderNews counts 245 start-ups in plant biotechnology alone.

Highflier Indigo Ag, a four-year-old start-up, raised more than $200 million in a fourth round of funding late last year. Indigo sells seeds coated with specialty microbes that improve row crop yields by helping plants shrug off drought and other stresses. The firm offers a per-bushel premium to farmers willing to adopt the new technology.

Large agriculture firms are also investing in technologies outside their traditional realms of seeds and chemicals. Bayer, for example, recently formed a company with the synthetic biology firm Ginkgo Bioworks to sell microbes that help plant roots fix nitrogen.

Automation may soon begin disrupting markets for traditional crop inputs like herbicides. FarmWise, a new start-up touting internet-connected robots, raised $5.7 million last month to commercialize weed-destroying robots that use computer vision technology to analyze each plant.

Pharmaceuticals

Drug industry strength to buoy fine chemicals makers

Pharmaceutical chemical firms such as AMRI, shown here in Rensselaer, N.Y., are benefiting from high drug approval rates.

Fine chemicals companies finished another strong year, and executives see strength following strength in 2018.

According to the Society of Chemical Manufacturers & Affiliates, a trade group representing fine and specialty chemical firms, sector sales volume increased 4.4% last year. The group expects comparable growth in 2018, thanks to product innovation in markets including pharmaceutical, agricultural, and industrial fine chemicals. For example, the U.S. Food & Drug Administration approved 46 drugs in 2017, more than twice as many as in 2016, and many of them are small molecules being manufactured by the fine chemicals industry.

Much of the growth in drug chemicals stems from customer needs for complex or highly potent molecules. The growth is spurring both investment and consolidation, according to producers. Indeed, the sector’s strong performance is attracting diversified companies such as PMC Group, which acquired two pharmaceutical chemical companies late last year.

“I continue to be bullish,” says Aslam Malik, CEO of Ampac Fine Chemicals. “More so this year because of tax reform.” The lowering of the corporate tax rate will encourage drug companies to invest in the U.S. and put U.S. fine chemicals firms in a stronger position to compete with Europe, he predicts.

Steven M. Klosk, CEO of the pharmaceutical chemical maker Cambrex, is also optimistic. “We continue to expect strong demand for CDMO outsourcing services,” he says, referring to contract development and manufacturing organizations. Klosk points to a global pipeline of over 5,000 small-molecule drugs in development.

While the sector appears to have broken from its traditional boom-and-bust cycle, some observers see certain types of bad behavior starting to recur. Consultant James Bruno, president of Chemical & Pharmaceutical Solutions, notes that the move of newcomers into the market is reminiscent of a similar failed rush some 15 years ago.

And the amassing of one-stop shops that combine pharmaceutical chemical and finished dosage manufacturing with other services works against the traditional business model of being small and specialized. “We are very cyclic,” Bruno says. “We do the same thing again and again. We screw up and we fix it. And we screw up again.”

Hydrocarbons and CO2 are winning the global battle to fill home refrigerators, says consultant Ray Will.

Persistent growth in the U.S., continued economic expansion in Asia, and a renewal of demand in Europe all bode well for specialty chemical output in 2018, according to the American Chemistry Council. The trade association projects a 3.0% global production rise in 2018 after a 2.5% increase in 2017.

Ever optimistic, ACC had expected output to jump 3.3% in 2017. But despite an overall pickup in the global economy, some industries that depend on specialty chemicals, such as oil and gas drilling, were weak, ACC says. Industry observers say the elements are in place for a better 2018.

Ray Will, a director at the consulting firm IHS Markit, discerns a number of trends likely to increase demand for specialty chemicals. Among them are a shift to electric vehicles and a move away from the use of fluorochemical coolants in home refrigerators.

China, Will says, plans to establish a system of quotas that will require electric vehicles to make up at least 10% of automakers’ output beginning in 2019 and increasing annually thereafter. The move is likely to bolster demand for battery materials as well as the electrolyte solutions that shuttle a charge between a battery’s anode and cathode.

Chemical makers could be in for a sweet ride if electric vehicles catch on in the U.S., points out credit rating agency Fitch Ratings. While Fitch sets the value of chemicals in a conventional vehicle at $3,000, it estimates the value of chemicals used in electric vehicles at $10,000, mostly related to batteries.

In the world of refrigeration, manufacturers are seeking coolants with low global warming potential. Rather than shift to hydrofluoroolefin refrigerants, many makers of home refrigerators, especially in Europe and Japan, are shifting to hydrocarbon refrigerants, Will says. The hydrofluoroolefins, developed for use in auto air-conditioning, are significantly more expensive, he notes.

The paints and coatings sector should benefit from an uptick in the economy, especially in the U.S., where tax reform will boost capital spending, predicts Phil Phillips, president of Chemark Consulting Group. New machinery and equipment, he says, require a significant amount of paint. Phillips expects paint production to rise about 3.5% in 2018.

Adhesives will grow at a similar rate, Phillips says, singling out a projected increase in demand for urethane adhesives to assemble and seal automobile body components.

Consumer demand for personal care chemicals continues to rise, according to the consulting firm Kline & Co. Trends in the $1.6 billion-per-year specialty ingredients market include growing demand for blue filters said to protect skin from computer screen emissions and cosmetics formulated to protect skin from air pollutants, says Kunal Mahajan, a chemicals project manager with Kline.

When it comes to investing in new chemical capacity, Canada has long dreamed big and delivered modestly. But that changed last month when Canadian firms green-lighted two large projects.

Canadian natural gas pipeline and processing firm Inter Pipeline approved the investment of $2.7 billion to build propane dehydrogenation (PDH) and polypropylene plants near Redwater, Alberta, by 2021.

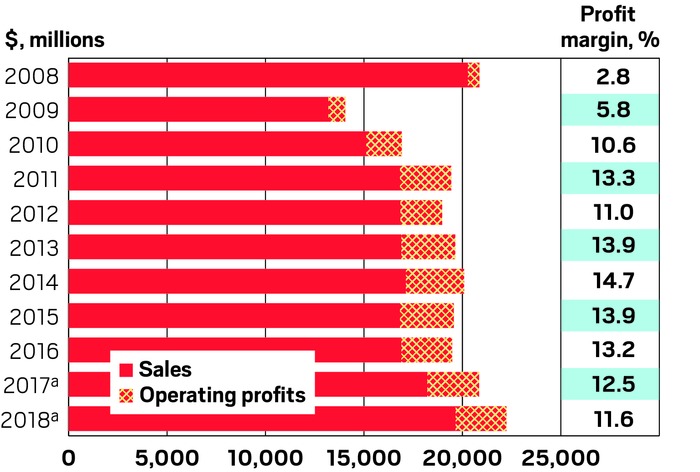

Canadian chemicals

The industry should have another strong year in 2018, though profitability may slip. a Projected. Note: Profit margin is operating profits as a percentage of sales.

Source: Chemistry Industry Association of Canada

Some 22,000 barrels per day of propane, half from Inter Pipeline’s own processing plant, will enter the facility; 525,000 metric tons per year of polypropylene will leave out the back.

The rationale for the facility is compelling, Inter Pipeline says. Because of a large surplus with no easy outlet to market, propane sells at a substantial discount in Alberta compared with the U.S. Gulf Coast. The company says the facility will be one of North America’s most competitive.

A joint venture between Pembina Pipeline and Petrochemical Industries Co. of Kuwait is set to reach a decision later this year on a similar PDH and polypropylene complex in Alberta.

Meanwhile, Canada’s largest chemical maker, Nova Chemicals, also approved a long-considered project last month. The company will build a 450,000-metric-ton-per-year polyethylene plant in Sarnia, Ontario, by 2021 and expand its cracker there by 50%.

All the projects are getting support from the government. Alberta is pitching in nearly $400 million in royalty credits for the PDH complexes. Ontario is contributing about $75 million toward Nova’s projects.

To Bob Masterson, president of the Chemistry Industry Association of Canada (CIAC), such incentives are a must if Canada is to attract investment. U.S. jurisdictions aren’t shy about offering packages to prospective investors, he observes.

“It has taken a lot of work to get everybody rowing their oars in the same direction, but we seem to be getting some results,” Masterson says, noting that projects worth billions more are under consideration.

The investments are coming at a time of growth for the Canadian chemical industry. In 2017, it saw sales increase by 7% to hit $20.8 billion, according to CIAC. Chemical makers surveyed by the group expect another 7% sales increase this year.

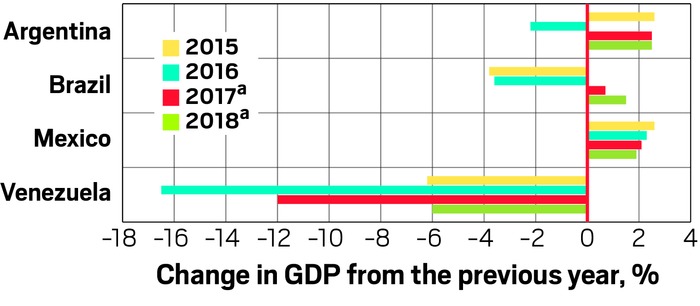

Latin America’s economic performance has been sluggish in recent years, with countries such as Brazil even dipping into recession. The past year, however, brought a turnaround for the region, and forecasters expect a return to growth in 2018.

Latin America’s economic performance has been sluggish in recent years, with countries such as Brazil even dipping into recession. The past year, however, brought a turnaround for the region, and forecasters expect a return to growth in 2018.

Course reversal

Argentina's and Brazil's economies turned around in 2017, but the recovery will be slow. a Projected. GDP = gross domestic product.

Source: International Monetary Fund

The positives for Latin America, according to economists at the Spanish bank BBVA, include rising commodity prices, currency devaluation leading to increased competitiveness, and a strong world economy. Last year was an “inflection point,” BBVA says, “after five years of slowdown and two (2015 and 2016) of contraction.”

After two recessionary years, Brazil’s economy, the region’s largest, is projected to post 0.7% growth for 2017, according to the International Monetary Fund. IMF analysts expect output to increase 1.5% in 2018. However, they caution that the Brazilian economy is still hampered by political uncertainty due to an upcoming presidential election and weak investment.

Chemical sales are showing signs of recovery. Brazilian giant Braskem reported that its polyethylene volumes increased by 4% in the first nine months of 2017 versus the year before. However, the firm’s sales of polyvinyl chloride (PVC), which is used by the construction sector for pipes and windows, were down by 3%.

Rina Quijada, a senior director and Latin America analyst for the consulting firm IHS Markit, says Brazilian demand for PVC has fallen 25% since 2015. She sees the market turning the corner in 2018 and demand climbing a modest 2%. Polyethylene demand will increase by 3%, she predicts.

Mexico is on track to grow by 1.9% this year, a slight slowdown from the 2.1% projected for 2017, according to IMF.

But the chemical industry there has a problem: raw material supply. Ever since Braskem and Grupo Idesa started up a $5 billion ethylene cracker in Nanchital, Mexico, in 2016, their contractual supplier of the raw material ethane, state oil company Pemex, hasn’t been able to scare up the ethane needed for its own facilities.

Pemex’s ethylene output has plunged 45% since 2015. Output of derivatives such as polyethylene, ethylene oxide, and styrene are also down sharply.

“It has been very difficult for Pemex to produce,” Quijada says. She notes that Pemex is evaluating options such as ethane imports from the U.S.

The engines of the U.S. economy are stoked to hum, if not roar, in 2018. Unemployment is low, consumer and business confidence is up, and corporations can look forward to lower tax rates. But recent years’ economic growth has not triggered a spike in U.S. chemical output, and it’s not clear that will change this year.

In 2017, the U.S. gross domestic product grew by 2.3%, but chemical output rose only 0.8%, much lower than the 3.8% predicted by the American Chemistry Council, the main U.S. chemical trade group. ACC now says 2018 will be the growth year, with output expanding 3.7%.

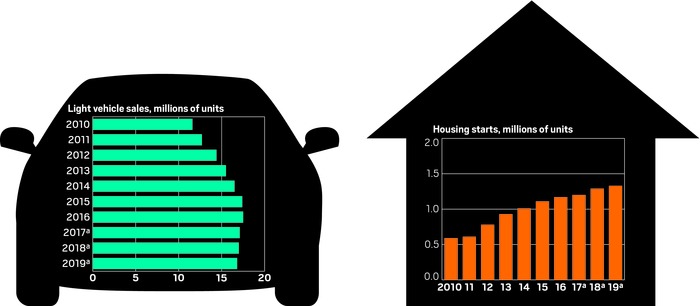

Building boom

While auto sales flatten, demand for housing will spur chemical sales.

a Projected.

Source: American Chemistry Council

A recent spate of capacity investment by U.S. industrial companies is good news for the chemical makers that supply them with raw materials. Overall, industrial firms increased capital spending by 8.7% in 2017 and will boost it an additional 2.7% this year, according to the Institute for Supply Management. ACC expects U.S. chemical companies to raise their capital spending 6.9% in 2018.

Another bright spot is home building. The strong jobs market and tight housing inventory caused a key index of builder confidence to jump in December. New construction permits soared by more than 15% compared with the end of 2016, according to Census Bureau data. ACC estimates that each new home requires about $15,000 worth of chemicals.

Auto manufacturing, in contrast, is not expected to add to demand for chemicals overall, though some specialties may see a lift. Sales last year were down from a peak of 17.5 million vehicles in 2016, and they are expected to remain flat.

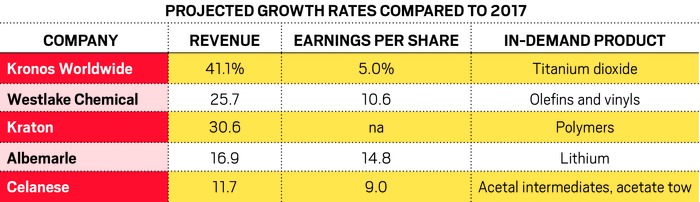

Big movers

Zacks Investment Research says these U.S. firms will benefit most from industrial demand.

na= not available..

Other chemical industry customers that ACC expects to grow this year include electronics, appliances, and aircraft parts. The oil and gas sector is expected to improve as oil reaches $55 per barrel. The downside is that chemical firms will see raw material and energy costs increase.

Overall, the global economy will expand by 3.8% in 2018 a bit faster than the expected U.S. rate of 2.6%, according to Deutsche Bank. Rising international demand will benefit U.S. chemical companies, which have a competitive advantage from low-cost shale gas. “With synchronous economic growth around the world, the global appetite for U.S. exports has increased,” says ACC economist T. Kevin Swift.

The capacity additions built to take advantage of the shale boom will continue to come on-line, and ACC expects the largest gains to happen this year and next. “In addition, a second wave of investment is on the way,” Swift says. “Much of the new production will be exported to customers around the world.”

Europe

With economic growth in the cards, confidence returns

In good shape: Europe’s chemical industry is poised to grow

2%: Anticipated sales growth in the EU in 2018

3%: Anticipated sales growth in Germany in 2018

3.1%: Growth in EU chemical production in the first half of 2017

84.1%: Plant capacity utilization, which has been growing for more than a year

5: Number of quarters that chemical business confidence has increased in Europe.

Source: Cefic

In good shape: Europe’s chemical industry is poised to grow

2%: Anticipated sales growth in the EU in 2018

3%: Anticipated sales growth in Germany in 2018

3.1%: Growth in EU chemical production in the first half of 2017

84.1%: Plant capacity utilization, which has been growing for more than a year

5: Number of quarters that chemical business confidence has increased in Europe.

Source: Cefic

Europe’s chemical industry has regained its confidence after economic recovery in the region, according to the European Chemical Industry Council (Cefic), a key chemical industry organization. Chemical output is set to increase 2% in 2018, after growing 3% across the European Union in 2017, Cefic says.

“The momentum is growing,” says Marco Mensink, Cefic’s director general. The growth will help the chemical industry step up investment in R&D and help the region transition to a resource-efficient, low-carbon, and circular economy, Mensink claims.

The cause is robust demand in sectors such as auto manufacturing, construction, metal fabrication, and electronics. Investments in new chemical production capacity are under way, Cefic says. Partly as a result, Europe’s chemical industry is now responsible for 1.1% of the EU’s gross domestic product and 1.2 million jobs, according to the association.

In Germany, the heartbeat of Europe’s chemical industry, the forecast is for chemical sales to rise 3% in 2018 to more than $230 billion. In 2017, Germany’s chemical sales increased more than 5%.

“We are confident that the upward trend will last next year,” said Kurt Bock, head of German chemical maker BASF, at an end-of-the-year press conference. “But where political aspects are concerned, we need to brace ourselves for persistently turbulent times.”

Despite the challenge of Brexit—Britain’s planned 2019 exit from the EU—the outlook for the U.K. chemical industry appears to be in line with the rest of Europe.

“We expect to see growth in 2018 … with a possibility it could be just under 2%,” says Stephen Elliott, CEO of the Chemical Industries Association, a U.K. trade group. The industry saw 3% growth in 2017.

But Elliott and Steve Bates, CEO of the BioIndustry Association, a biotech group, remain concerned about the potential impact of Brexit. They are calling for the U.K. government to put in place measures that will enable their respective sectors to continue trading with the EU.

Even if such measures are established, U.K. chemical companies will likely take a hit, according to Paul Hodges, chairman of the London-based consulting firm International eChem. European customers of British chemical firms, he says, will be asking whether they can find another supplier or producer outside the U.K.

Asia

Despite financial risks, region is looking at another banner year

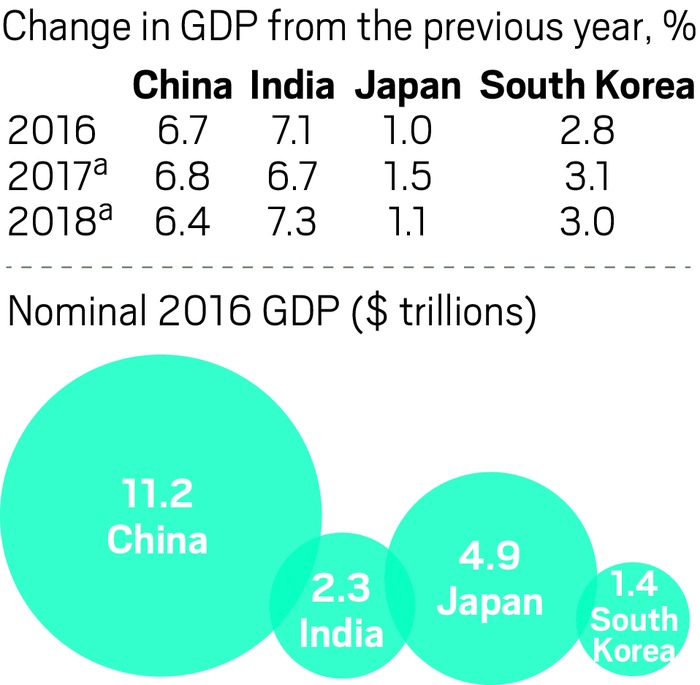

India and China matched growth in 2017, but India is expected to take the lead again this year. a Projected. GDP = gross domestic product.

Sources: Asian Development Bank, World Bank

Demand for chemicals is steady in China, Japanese chemical companies are upgrading their profit forecasts, and economic growth is accelerating in India. In sum: The outlook for the Asian chemical industry in 2018 is good.

Predictions of strong economic growth in China, India, and Indonesia translate to “a positive outlook for the Asian chemical industry as a whole,” says Steve Jenkins, vice president of chemicals consulting at market research firm PCI Wood Mackenzie.

In Japan, the economy will not be that strong, but chemical companies will be able to grow their margins by focusing on technologically advanced materials, Jenkins says. The continued weakness of the yen will raise profits in yen terms, he adds.

In China, the world’s largest market for chemicals, consumer demand is buoying chemical production, Jenkins notes. The widespread use of smartphones to order from online retailers, for instance, is stimulating demand for consumer goods in once-stagnant inland provinces.

Meanwhile, strict enforcement of environmental regulations is changing China’s chemical industry, Jenkins notes, in part by leading many firms to upgrade their facilities to stay in business.

Environmental controls are having a wide impact, agrees Peter Huo, vice president for sales and marketing at the Chinese polyurethane chemicals producer Wanhua Chemical.

Even when their operations are compliant, Wanhua and its competitors have had to cut production as a result of China’s crackdown. Wanhua, for example, had to temporarily reduce production at some of its plants because “some of the buyers of our products had to stop theirs,” Huo explains.

But on the whole, Chinese demand for polyurethane materials and other chemicals was steady in 2017, a trend that Huo expects to continue for at least the first half of 2018. The combination of constant demand and lowered supply due to the crackdown is boosting profit margins, he notes.

The main risks facing Asia are financial. A major slowdown of the U.S. stock market could “derail the current buoyant mood,” Jenkins warns. And government officials in China are mentioning more often the need to reduce debt levels in both the private and public sectors, a shift that could dampen the economy as a whole by reducing funds available to invest or expand, Huo says.

6%: Share of global production, up from 3% in 2000

102: Number of products being made

159 million metric tons: Production, up 8.5% since 2015

$91 billion: Sales, down 3% since 2015

$584 million: R&D spending, down 20% since 2015

49%: Share of Gulf production attributable to Saudi Arabia

Note: Figures are for 2016 Source:GPCA

Middle East chemicals by the numbers

6%: Share of global production, up from 3% in 2000

102: Number of products being made

159 million metric tons: Production, up 8.5% since 2015

$91 billion: Sales, down 3% since 2015

$584 million: R&D spending, down 20% since 2015

49%: Share of Gulf production attributable to Saudi Arabia

Note: Figures are for 2016 Source:GPCA

With oil prices widely tipped to stay around $60 per barrel or lower for the next few years, the low-cost-energy advantage enjoyed by the Middle East’s chemical sector will continue to evaporate, experts say. As this scenario becomes the new normal, many Middle Eastern chemical companies see 2018 as the year they must shift faster away from basic petrochemicals and toward higher-value specialty products.

“One thing we know for certain: The status quo is not an option,” Yousef Al-Benyan, chairman of the Gulf Petrochemicals & Chemicals Association and CEO of the big Saudi firm SABIC, told delegates at the GPCA Annual Forum late last year. “The fundamental change required to deliver a quantum leap in performance is transformation; it is not an incremental improvement.”

In addition to the low price of oil, challenges the region faces include lower profit margins, China’s rise to self-sufficiency, and the shale-enabled chemical expansion in the U.S., Al-Benyan said.

The fundamental change required to deliver a quantum leap in performance is transformation; it is not an incremental improvement.

—Yousef Al-Benyan, chairman of the Gulf Petrochemicals & Chemicals Association (GPCA)

Using mergers and acquisitions is one way Middle Eastern companies could improve their difficult position, says Mirko Rubeis, a managing director of Boston Consulting Group. He says companies in the Gulf Cooperative Council region—which includes the lion’s share of the Middle East’s chemical industry—should strive to focus their portfolios in areas such as specialty chemicals while reducing costs through economies of scale.

Sadara by the numbers

6 years: Time it took to construct Sadara, a joint venture between Dow Chemical and Saudi Aramco

3 million metric tons per year: Amount of chemicals and plastics being produced at the site

26: Number of plants at the site

Sept. 17, 2017: The day Sadara commissioned its final plant, a toluene diisocyanate facility

160,000 metric tons: Amount of steel needed to construct the site

2,500 km: Length of piping at the site

Source: Sadara

Sadara by the numbers

6 years: Time it took to construct Sadara, a joint venture between Dow Chemical and Saudi Aramco

3 million metric tons per year: Amount of chemicals and plastics being produced at the site

26: Number of plants at the site

Sept. 17, 2017: The day Sadara commissioned its final plant, a toluene diisocyanate facility

160,000 metric tons: Amount of steel needed to construct the site

2,500 km: Length of piping at the site

Source: Sadara

It’s a view echoed by H. E. Khalid A. Al-Falih, Saudi Arabia’s minister of energy, industry, and mineral resources and chair of Saudi Aramco. Speaking at the GPCA forum, he called on regional players to think globally and on governments to adopt policies that encourage venture capital investment and greater spending on R&D.

Dow Chemical and Saudi Aramco point to their Sadara Chemical Company joint venture as an example of how to integrate the Middle East’s basic chemicals prowess with high-end production of specialty materials.

Last year, Sadara started up a polyurethane raw material plant at its complex in Jubail, Saudi Arabia. It is the last of 26 facilities to be commissioned at the $20 billion site. A raft of downstream facilities—such as a plastics processing plant—are now being built nearby.

Rejecting the downbeat outlook of others producing chemicals in the Middle East, DowDuPont executive chairman Andrew N. Liveris has pledged that he will continue to make specialty chemical investments in the region. For Liveris, at least, the Middle East is still a land of opportunity.